Let’s dig into the relative performance of FormFactor (NASDAQ: FORM) and its peers as we unravel the now-completed Q4 semiconductor manufacturing earnings season.

The semiconductor industry is driven by demand for advanced electronic products like smartphones, PCs, servers, and data storage. The need for technologies like artificial intelligence, 5G networks, and smart cars is also creating the next wave of growth for the industry. Keeping up with this dynamism requires new tools that can design, fabricate, and test chips at ever smaller sizes and more complex architectures, creating a dire need for semiconductor capital manufacturing equipment.

The 14 semiconductor manufacturing stocks we track reported a very strong Q4. As a group, revenues beat analysts’ consensus estimates by 3% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady as they are up 1.3% on average since the latest earnings results.

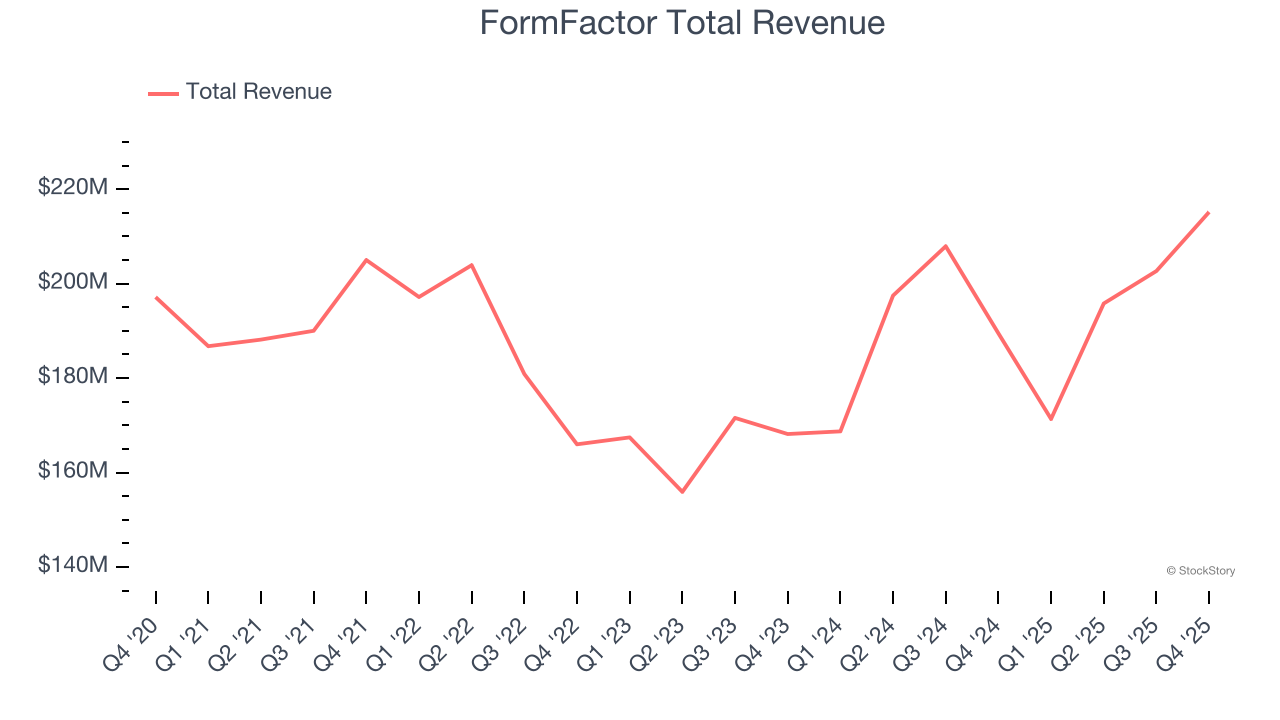

FormFactor (NASDAQ: FORM)

With customers across the foundry and fabless markets, FormFactor (NASDAQ: FORM) is a US-based provider of test and measurement technologies for semiconductors.

FormFactor reported revenues of $215.2 million, up 13.6% year on year. This print exceeded analysts’ expectations by 2.3%. Overall, it was an exceptional quarter for the company with a beat of analysts’ EPS estimates and an impressive beat of analysts’ adjusted operating income estimates.

“FormFactor’s fourth quarter revenue, gross margin, and earnings per share all exceeded both third quarter results and the high end of our outlook range, and we posted record revenue on both a quarterly and annual basis,” said Mike Slessor, CEO of FormFactor, Inc.

Interestingly, the stock is up 32.2% since reporting and currently trades at $94.62.

Is now the time to buy FormFactor? Access our full analysis of the earnings results here, it’s free.

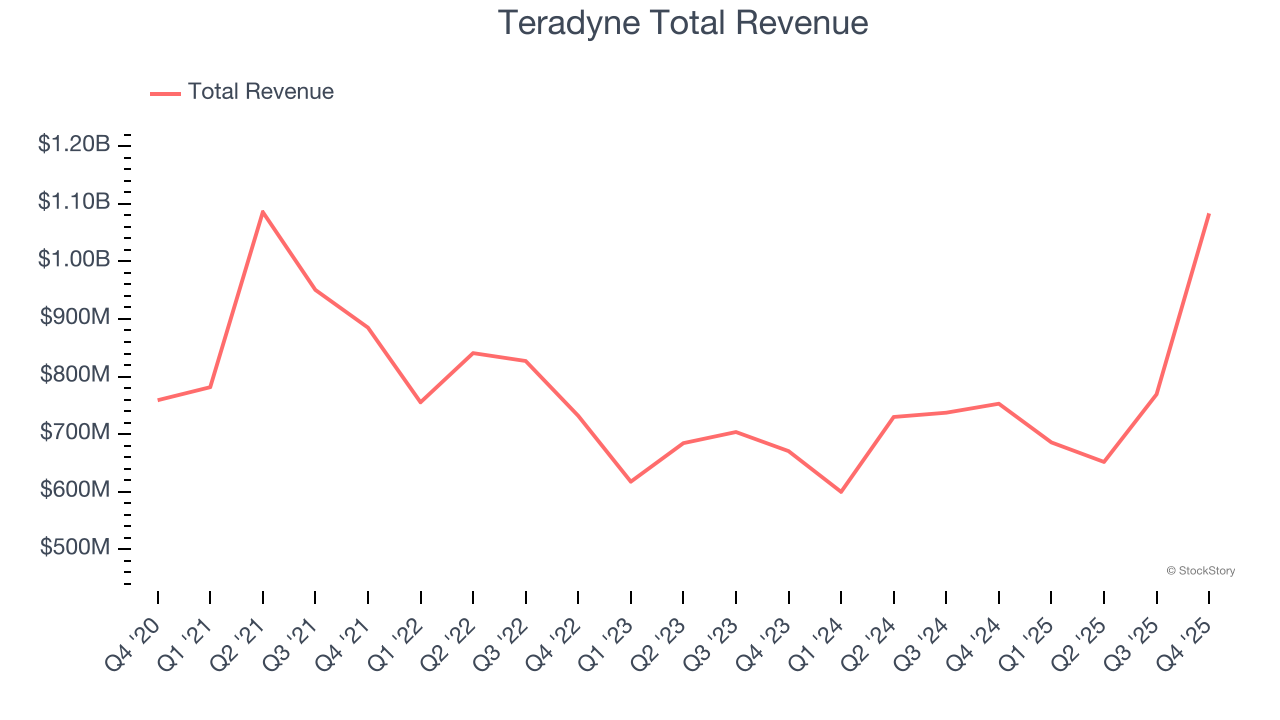

Best Q4: Teradyne (NASDAQ: TER)

Sporting most major chip manufacturers as its customers, Teradyne (NASDAQ: TER) is a US-based supplier of automated test equipment for semiconductors as well as other technologies and devices.

Teradyne reported revenues of $1.08 billion, up 43.9% year on year, outperforming analysts’ expectations by 11%. The business had an incredible quarter with a significant improvement in its inventory levels and a beat of analysts’ EPS estimates.

Teradyne pulled off the biggest analyst estimates beat and fastest revenue growth among its peers. The market seems happy with the results as the stock is up 19.5% since reporting. It currently trades at $298.17.

Is now the time to buy Teradyne? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Amtech (NASDAQ: ASYS)

Focusing on the silicon carbide and power semiconductor sectors, Amtech Systems (NASDAQ: ASYS) produces the machinery and related chemicals needed for manufacturing semiconductors.

Amtech reported revenues of $18.97 million, down 22.2% year on year, in line with analysts’ expectations. It was a slower quarter as it posted a significant miss of analysts’ EPS estimates and an increase in its inventory levels.

Amtech delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 31.6% since the results and currently trades at $10.85.

Read our full analysis of Amtech’s results here.

Applied Materials (NASDAQ: AMAT)

Founded in 1967 as the first company to develop tools for other businesses in the semiconductor industry, Applied Materials (NASDAQ: AMAT) is the largest provider of semiconductor wafer fabrication equipment.

Applied Materials reported revenues of $7.01 billion, down 2.1% year on year. This result beat analysts’ expectations by 1.8%. It was an exceptional quarter as it also recorded revenue guidance for next quarter exceeding analysts’ expectations and a beat of analysts’ EPS estimates.

The stock is up 7.6% since reporting and currently trades at $353.19.

Read our full, actionable report on Applied Materials here, it’s free.

Marvell Technology (NASDAQ: MRVL)

Moving away from a low margin storage device management chips in one of the biggest semiconductor business model pivots of the past decade, Marvell Technology (NASDAQ: MRVL) is a fabless designer of special purpose data processing and networking chips used by data centers, communications carriers, enterprises, and autos.

Marvell Technology reported revenues of $2.22 billion, up 22.1% year on year. This number topped analysts’ expectations by 0.5%. More broadly, it was a satisfactory quarter as it also produced revenue guidance for next quarter beating analysts’ expectations but an increase in its inventory levels.

The stock is up 19.9% since reporting and currently trades at $90.76.

Read our full, actionable report on Marvell Technology here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.