Looking back on consumer finance stocks’ Q4 earnings, we examine this quarter’s best and worst performers, including Credit Acceptance (NASDAQ: CACC) and its peers.

Consumer finance companies provide loans and credit products to individuals. Growth drivers include increasing consumer spending, financial inclusion initiatives in developing markets, and digital lending platforms reducing distribution costs. Challenges include credit risk during economic downturns, regulatory scrutiny of lending practices, and intensifying competition from traditional banks and fintech firms offering innovative credit solutions.

The 19 consumer finance stocks we track reported a satisfactory Q4. As a group, revenues missed analysts’ consensus estimates by 0.7% while next quarter’s revenue guidance was 0.9% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 8.3% since the latest earnings results.

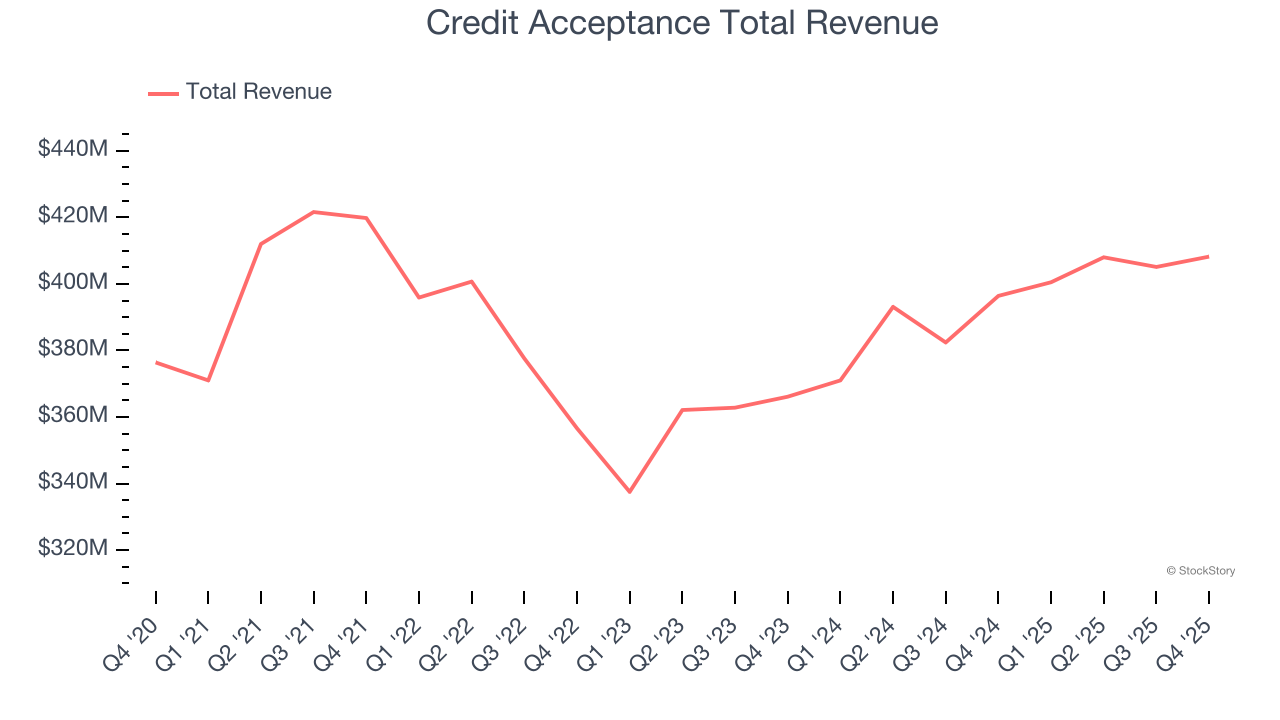

Credit Acceptance (NASDAQ: CACC)

Founded in 1972 by Donald Foss to serve customers overlooked by traditional lenders, Credit Acceptance (NASDAQ: CACC) provides auto financing solutions that enable car dealers to sell vehicles to consumers with limited or impaired credit histories.

Credit Acceptance reported revenues of $408.2 million, up 3% year on year. This print fell short of analysts’ expectations by 12.1%. Overall, it was a slower quarter for the company with a significant miss of analysts’ revenue estimates.

“We are pleased to announce sequential growth in our financial results in the fourth quarter of 2025,” said Vinayak Hegde, CEO of Credit Acceptance.

Credit Acceptance delivered the weakest performance against analyst estimates of the whole group. Interestingly, the stock is up 11% since reporting and currently trades at $500.86.

Read our full report on Credit Acceptance here, it’s free.

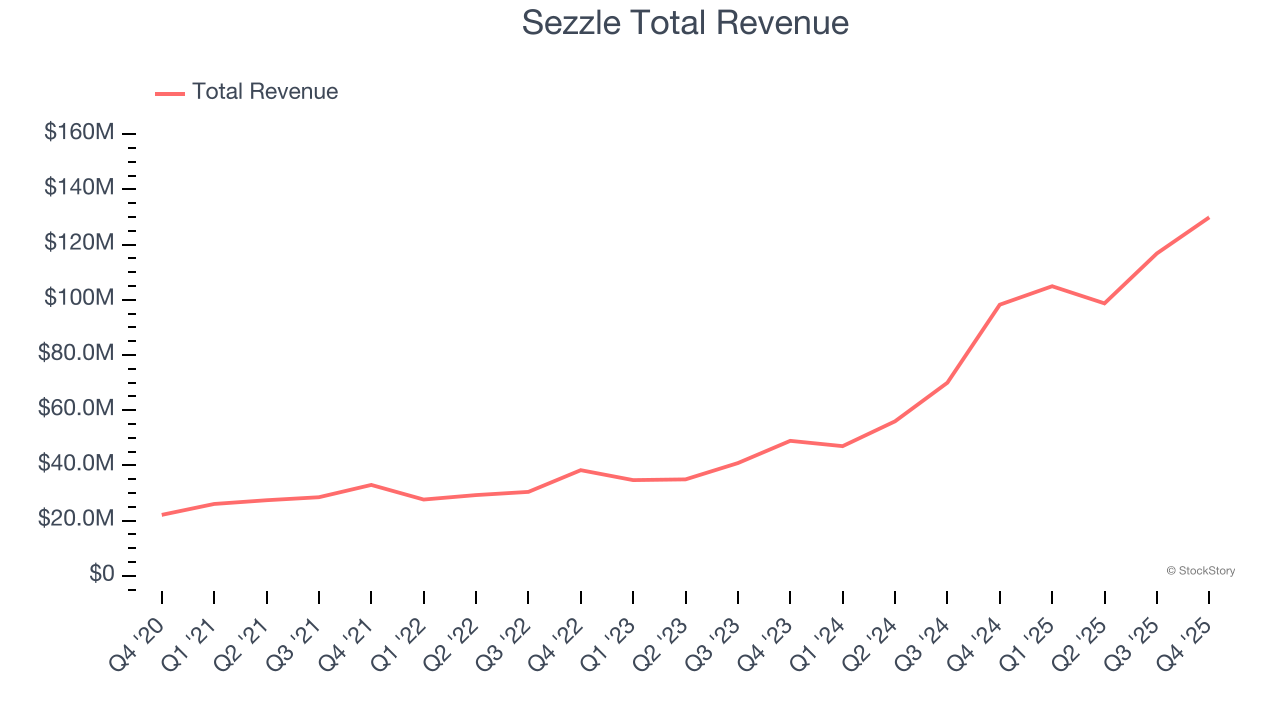

Best Q4: Sezzle (NASDAQ: SEZL)

Founded in 2016 as an alternative to traditional credit cards for younger shoppers, Sezzle (NASDAQ: SEZL) provides a payment platform that allows consumers to split purchases into four interest-free installments over six weeks at participating retailers.

Sezzle reported revenues of $129.9 million, up 32.2% year on year, outperforming analysts’ expectations by 2.7%. The business had an exceptional quarter with a beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

The market seems happy with the results as the stock is up 14.9% since reporting. It currently trades at $71.94.

Is now the time to buy Sezzle? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Navient (NASDAQ: NAVI)

Spun off from Sallie Mae in 2014 to handle the company's loan servicing and collection operations, Navient (NASDAQ: NAVI) provides education loan servicing and business processing solutions that help manage federal student loans, private education loans, and government services.

Navient reported revenues of $144 million, down 11.7% year on year, falling short of analysts’ expectations by 7.6%. It was a disappointing quarter as it posted a significant miss of analysts’ net interest income estimates and a significant miss of analysts’ revenue estimates.

Navient delivered the slowest revenue growth in the group. As expected, the stock is down 31.5% since the results and currently trades at $8.25.

Read our full analysis of Navient’s results here.

Dave (NASDAQ: DAVE)

Named after the biblical David fighting financial Goliaths, Dave (NASDAQ: DAVE) is a digital financial services platform that helps Americans living paycheck to paycheck with cash advances, banking services, and tools to improve their financial health.

Dave reported revenues of $163.7 million, up 62.4% year on year. This number beat analysts’ expectations by 0.9%. Overall, it was a strong quarter as it also produced full-year revenue guidance exceeding analysts’ expectations and an impressive beat of analysts’ revenue estimates.

Dave pulled off the fastest revenue growth and highest full-year guidance raise among its peers. The stock is up 9.6% since reporting and currently trades at $218.13.

Read our full, actionable report on Dave here, it’s free.

Capital One (NYSE: COF)

Starting as a credit card company in 1988 before expanding into a full-service bank, Capital One (NYSE: COF) is a financial services company that offers credit cards, auto loans, banking services, and commercial lending to consumers and businesses.

Capital One reported revenues of $15.62 billion, up 53.3% year on year. This result surpassed analysts’ expectations by 0.9%. Zooming out, it was a slower quarter as it logged a significant miss of analysts’ EPS estimates and a miss of analysts’ net interest margin estimates.

The stock is down 21.2% since reporting and currently trades at $185.35.

Read our full, actionable report on Capital One here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.