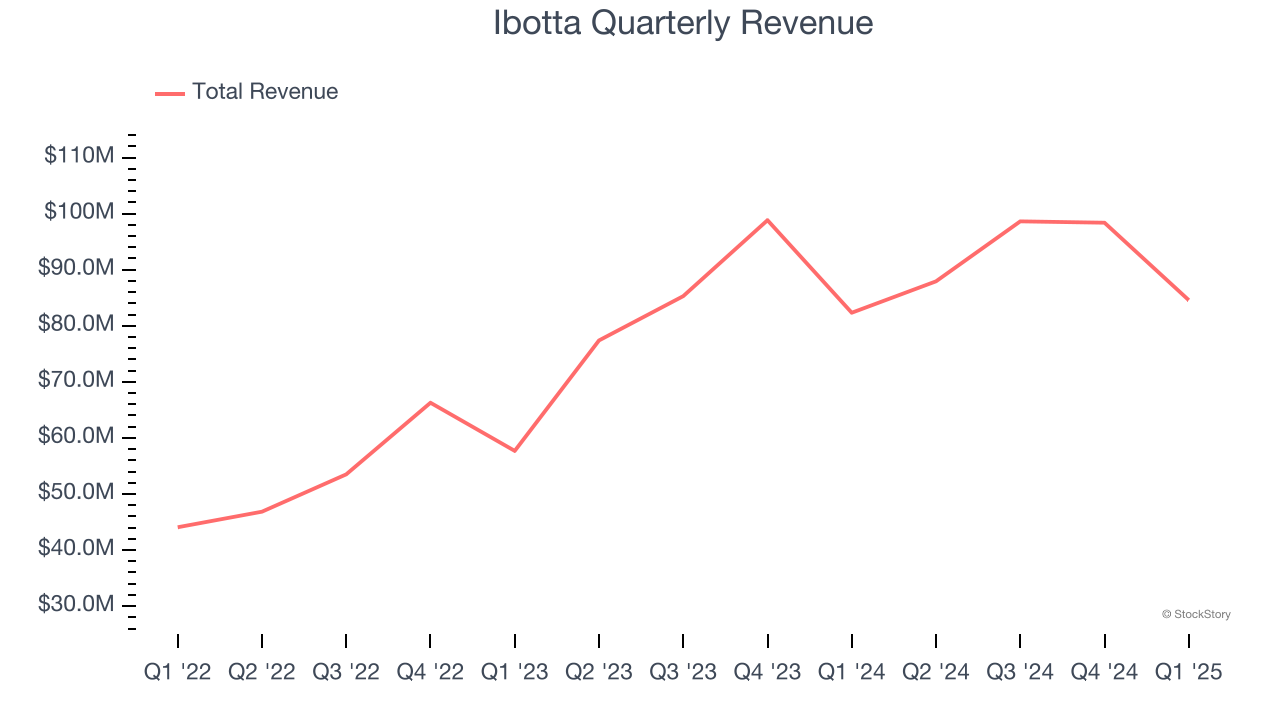

Cash-back rewards platform Ibotta (NYSE: IBTA) reported revenue ahead of Wall Street’s expectations in Q1 CY2025, with sales up 2.7% year on year to $84.57 million. The company expects next quarter’s revenue to be around $89.5 million, close to analysts’ estimates. Its non-GAAP profit of $0.36 per share was 7.8% below analysts’ consensus estimates.

Is now the time to buy Ibotta? Find out by accessing our full research report, it’s free.

Ibotta (IBTA) Q1 CY2025 Highlights:

- Revenue: $84.57 million vs analyst estimates of $82.06 million (2.7% year-on-year growth, 3.1% beat)

- Adjusted EPS: $0.36 vs analyst expectations of $0.39 (7.8% miss)

- Adjusted EBITDA: $14.67 million vs analyst estimates of $12.56 million (17.3% margin, 16.8% beat)

- Revenue Guidance for Q2 CY2025 is $89.5 million at the midpoint, roughly in line with what analysts were expecting

- EBITDA guidance for Q2 CY2025 is $19.5 million at the midpoint, in line with analyst expectations

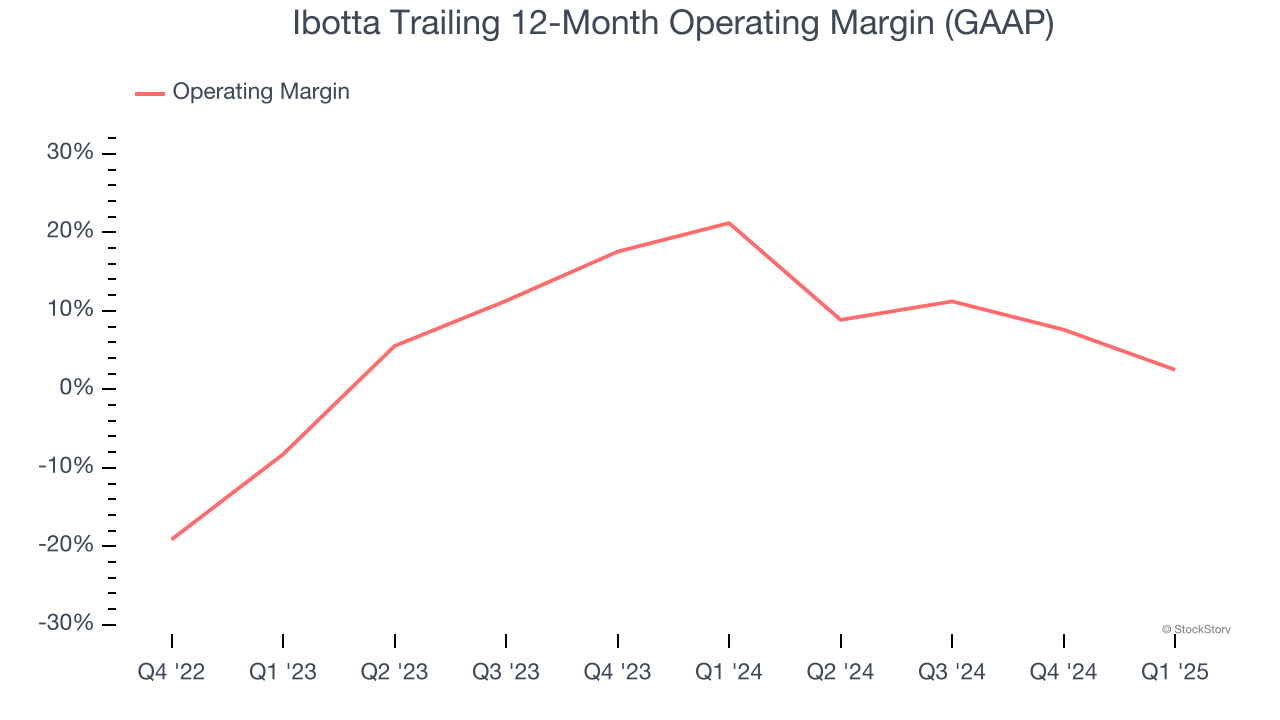

- Operating Margin: -3.3%, down from 19.3% in the same quarter last year

- Free Cash Flow Margin: 17.6%, down from 20.5% in the same quarter last year

- Market Capitalization: $1.47 billion

“We made significant progress in the first quarter in establishing Ibotta as the first full-service performance marketing platform for the CPG industry,” said Ibotta CEO and founder, Bryan Leach.

Company Overview

Originally launched as a way to make grocery shopping more rewarding for budget-conscious consumers, Ibotta (NYSE: IBTA) is a mobile shopping app that allows consumers to earn cash back on everyday purchases by completing tasks and submitting receipts.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $369.5 million in revenue over the past 12 months, Ibotta is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

As you can see below, Ibotta’s 28.3% annualized revenue growth over the last two years was incredible. This is a great starting point for our analysis because it shows Ibotta’s demand was higher than many business services companies.

This quarter, Ibotta reported modest year-on-year revenue growth of 2.7% but beat Wall Street’s estimates by 3.1%. Company management is currently guiding for a 1.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6% over the next 12 months, a deceleration versus the last two years. Still, this projection is above average for the sector and suggests the market sees some success for its newer products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Ibotta’s operating margin has been trending down over the last 12 months and averaged 4.2% over the last three years. Although this result isn’t good, the company’s elite historical revenue growth suggests it ramped up investments to capture market share. We’ll keep a close eye to see if this strategy pays off.

This quarter, Ibotta generated an operating profit margin of negative 3.3%, down 22.6 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

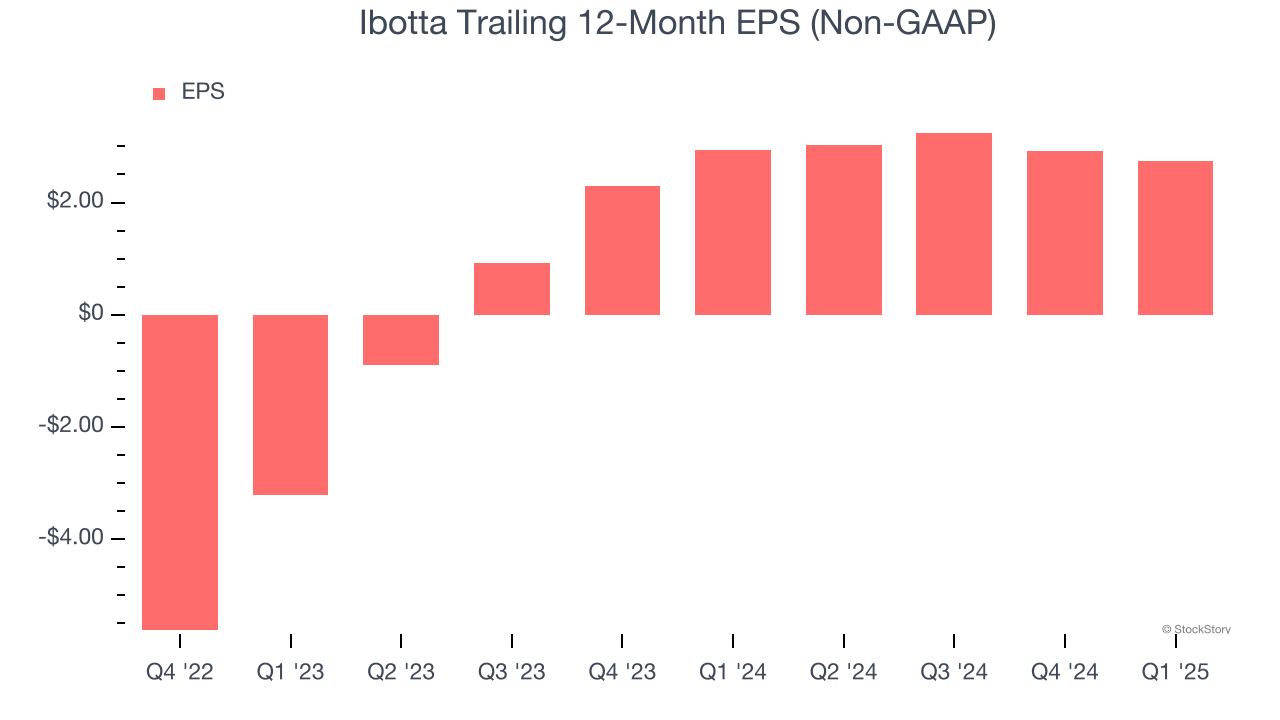

Ibotta’s full-year EPS flipped from negative to positive over the last two years. This is a good sign and shows it’s at an inflection point.

In Q1, Ibotta reported EPS at $0.36, down from $0.54 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Ibotta’s Q1 Results

We enjoyed seeing Ibotta beat analysts’ revenue and EBITDA expectations this quarter. On the other hand, its EPS missed. Overall, this was a mixed quarter. The stock traded up 12.7% to $56.61 immediately after reporting.

Big picture, is Ibotta a buy here and now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.