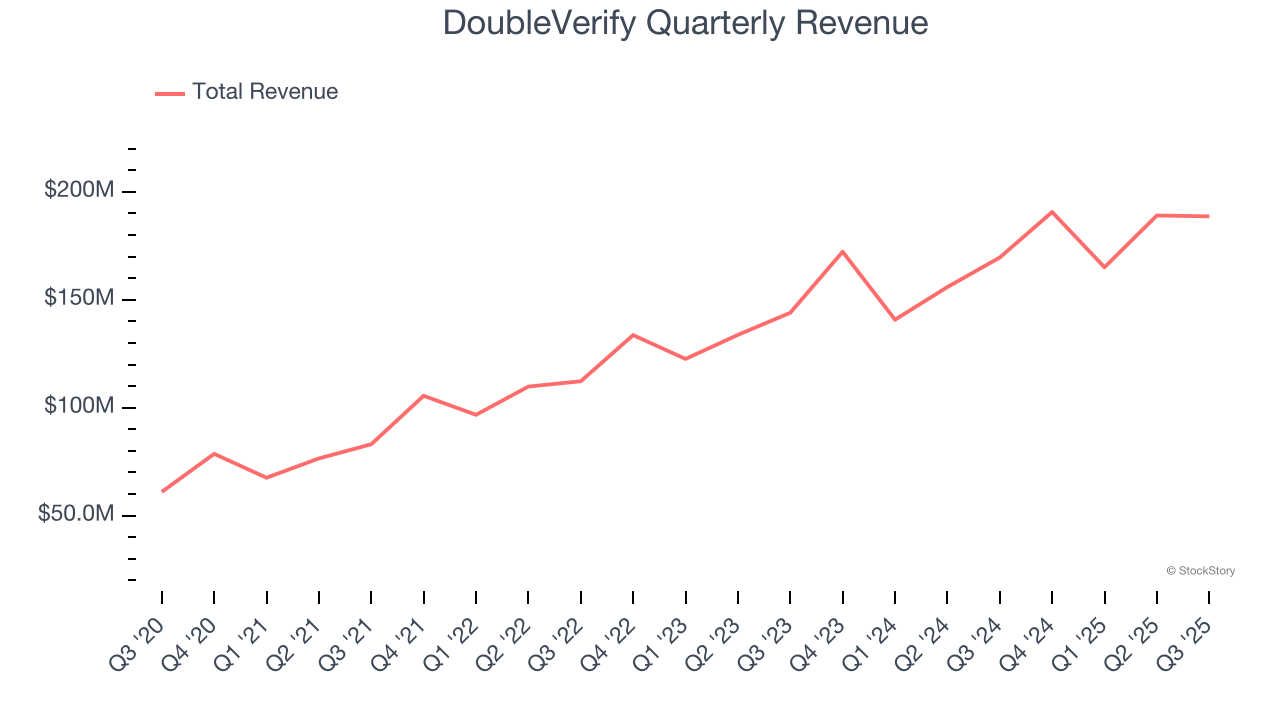

Digital ad verification company DoubleVerify (NYSE: DV) fell short of the markets revenue expectations in Q3 CY2025, but sales rose 11.2% year on year to $188.6 million. Next quarter’s revenue guidance of $209 million underwhelmed, coming in 0.9% below analysts’ estimates. Its non-GAAP profit of $0.22 per share was 17.4% below analysts’ consensus estimates.

Is now the time to buy DoubleVerify? Find out by accessing our full research report, it’s free for active Edge members.

DoubleVerify (DV) Q3 CY2025 Highlights:

- Revenue: $188.6 million vs analyst estimates of $190.2 million (11.2% year-on-year growth, 0.8% miss)

- Adjusted EPS: $0.22 vs analyst expectations of $0.27 (17.4% miss)

- Adjusted EBITDA: $65.85 million vs analyst estimates of $62.2 million (34.9% margin, 5.9% beat)

- Revenue Guidance for Q4 CY2025 is $209 million at the midpoint, below analyst estimates of $210.8 million

- EBITDA guidance for Q4 CY2025 is $79 million at the midpoint, above analyst estimates of $77.86 million

- Operating Margin: 11.2%, down from 15.2% in the same quarter last year

- Free Cash Flow Margin: 20.7%, similar to the previous quarter

- Market Capitalization: $1.80 billion

Company Overview

Using advanced analytics to evaluate over 17 billion digital ad transactions daily, DoubleVerify (NYSE: DV) provides AI-powered technology that verifies digital ads are viewable, fraud-free, brand-suitable, and displayed in the intended geographic location.

Revenue Growth

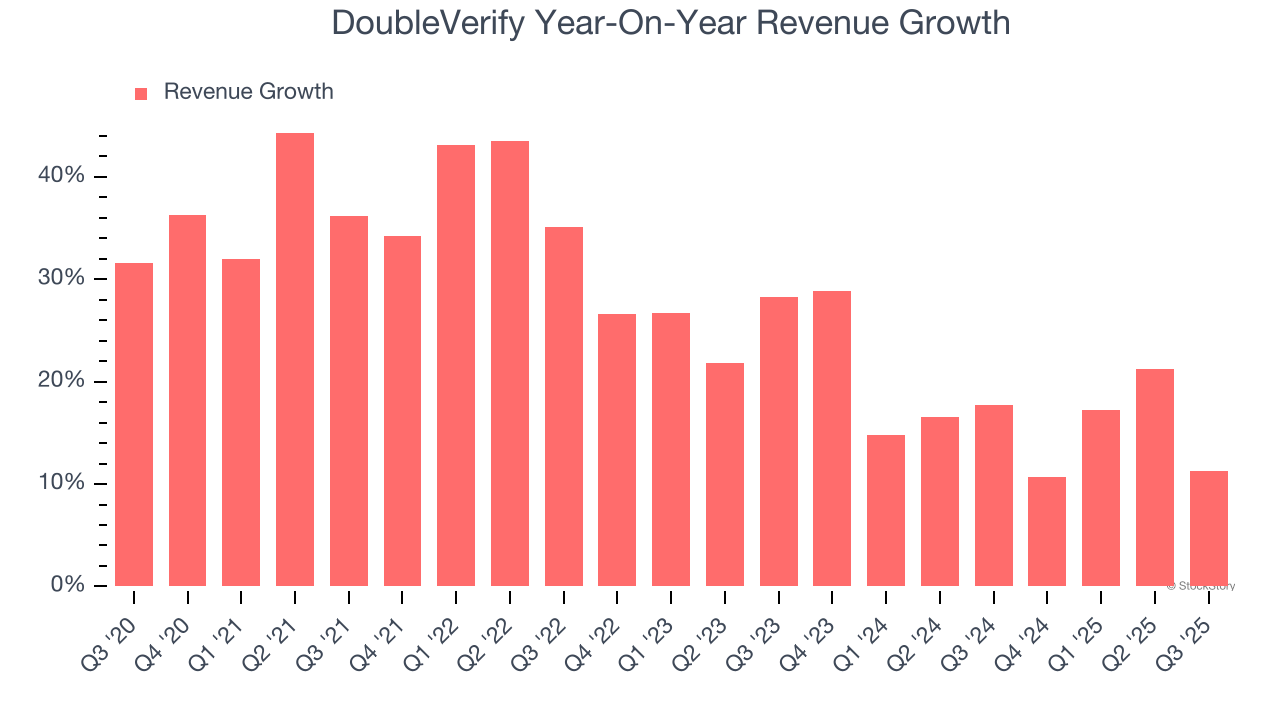

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, DoubleVerify’s 26.9% annualized revenue growth over the last five years was impressive. Its growth beat the average software company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. DoubleVerify’s annualized revenue growth of 17.2% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, DoubleVerify’s revenue grew by 11.2% year on year to $188.6 million but fell short of Wall Street’s estimates. Company management is currently guiding for a 9.6% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 10.5% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

DoubleVerify’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a competitive market and must continue investing to grow.

Key Takeaways from DoubleVerify’s Q3 Results

We enjoyed seeing DoubleVerify beat analysts’ EBITDA expectations this quarter. We were also glad its EBITDA guidance for next quarter slightly exceeded Wall Street’s estimates. On the other hand, its revenue guidance for next quarter slightly missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 7.6% to $10.13 immediately after reporting.

DoubleVerify didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.