Regional banking company Prosperity Bancshares (NYSE: PB) missed Wall Street’s revenue expectations in Q3 CY2025 as sales rose 3.9% year on year to $314.7 million. Its GAAP profit of $1.45 per share was in line with analysts’ consensus estimates.

Is now the time to buy Prosperity Bancshares? Find out by accessing our full research report, it’s free for active Edge members.

Prosperity Bancshares (PB) Q3 CY2025 Highlights:

- Net Interest Income: $273.4 million vs analyst estimates of $276.9 million (4.5% year-on-year growth, 1.2% miss)

- Net Interest Margin: 3.2% vs analyst estimates of 3.3% (in line)

- Revenue: $314.7 million vs analyst estimates of $317.5 million (3.9% year-on-year growth, 0.9% miss)

- Efficiency Ratio: 44.1% vs analyst estimates of 44.3% (28.5 basis point beat)

- EPS (GAAP): $1.45 vs analyst estimates of $1.44 (in line)

- Tangible Book Value per Share: $43.23 vs analyst estimates of $43.27 (8.8% year-on-year growth, in line)

- Market Capitalization: $6.01 billion

"In the third quarter we signed a definitive merger agreement with Southwest Bancshares, Inc., the parent company of Texas Partners Bank headquartered in San Antonio, Texas. We are excited about this transaction as it significantly expands our San Antonio metro footprint with 4 additional branches and increased deposit market share, bolsters our presence in the Texas Hill Country and adds an experienced C&I lending team," said David Zalman, Prosperity's Senior Chairman and Chief Executive Officer.

Company Overview

With a network of banking centers spanning the Lone Star State and beyond, Prosperity Bancshares (NYSE: PB) operates full-service banking locations throughout Texas and Oklahoma, offering a wide range of financial products and services to businesses and consumers.

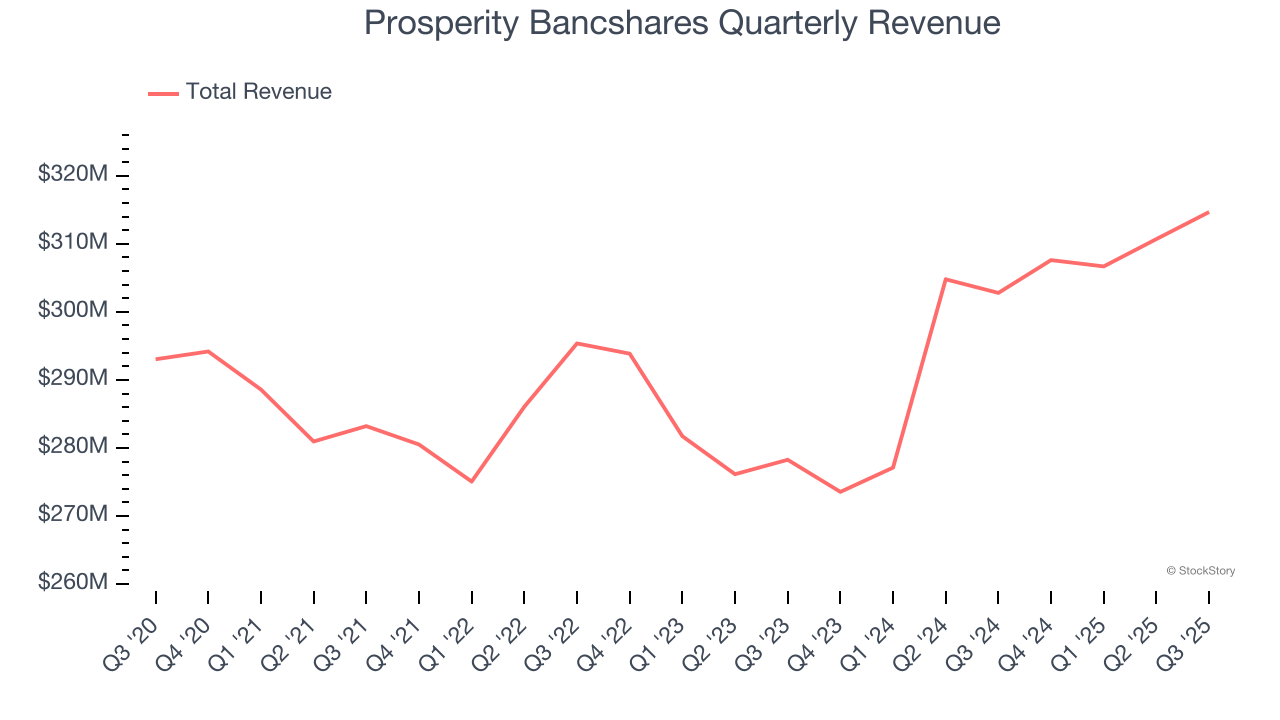

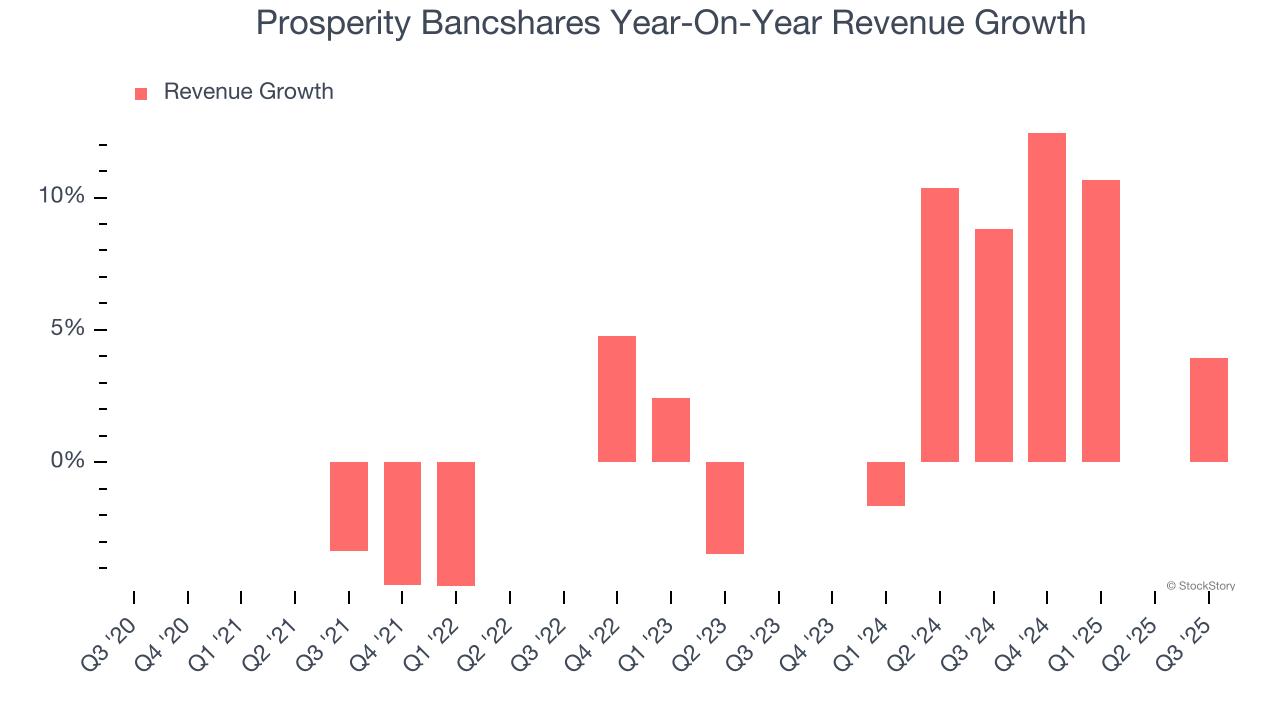

Sales Growth

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions. Regrettably, Prosperity Bancshares’s revenue grew at a tepid 1.8% compounded annual growth rate over the last five years. This fell short of our benchmarks and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Prosperity Bancshares’s annualized revenue growth of 4.7% over the last two years is above its five-year trend, but we were still disappointed by the results.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Prosperity Bancshares’s revenue grew by 3.9% year on year to $314.7 million, falling short of Wall Street’s estimates.

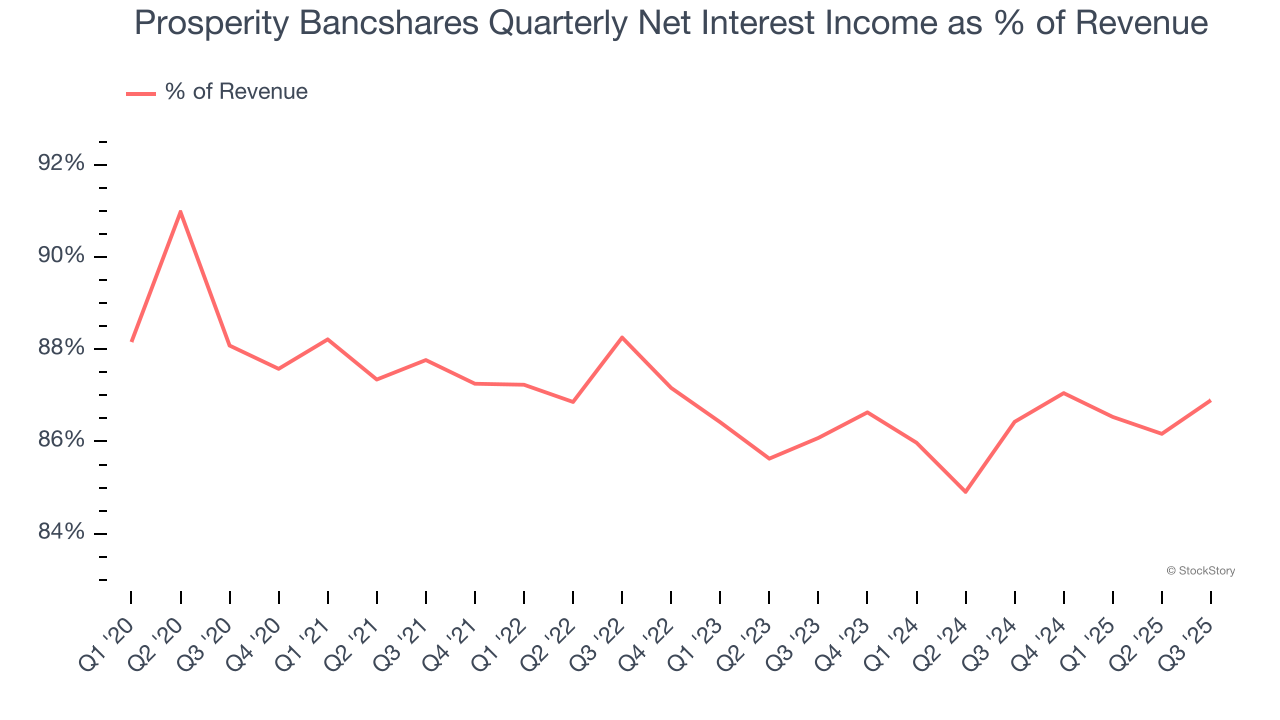

Net interest income made up 86.8% of the company’s total revenue during the last five years, meaning Prosperity Bancshares barely relies on non-interest income to drive its overall growth.

Our experience and research show the market cares primarily about a bank’s net interest income growth as non-interest income is considered a lower-quality and non-recurring revenue source.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

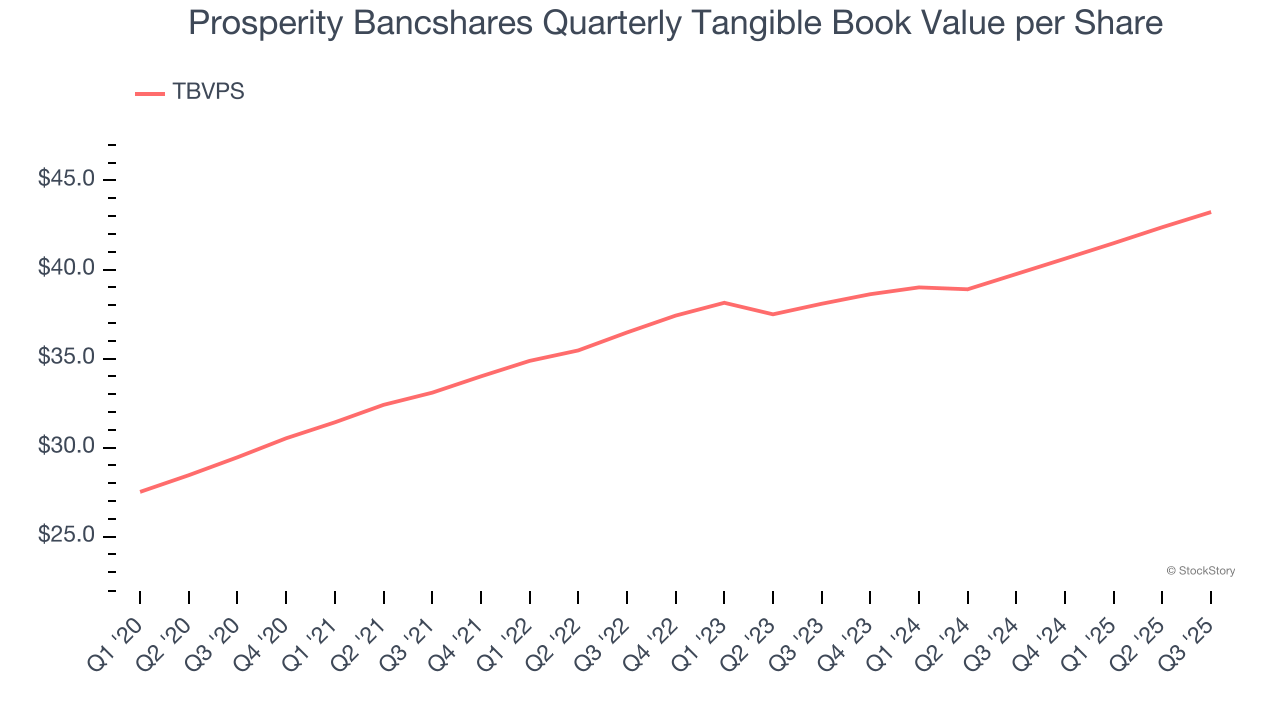

Tangible Book Value Per Share (TBVPS)

Banks are balance sheet-driven businesses because they generate earnings primarily through borrowing and lending. They’re also valued based on their balance sheet strength and ability to compound book value (another name for shareholders’ equity) over time.

When analyzing banks, tangible book value per share (TBVPS) takes precedence over many other metrics. This measure isolates genuine per-share value by removing intangible assets of debatable liquidation worth. Other (and more commonly known) per-share metrics like EPS can sometimes be murky due to M&A or accounting rules allowing for loan losses to be spread out.

Prosperity Bancshares’s TBVPS grew at an impressive 8% annual clip over the last five years. However, TBVPS growth has recently decelerated a bit to 6.5% annual growth over the last two years (from $38.08 to $43.23 per share).

Over the next 12 months, Consensus estimates call for Prosperity Bancshares’s TBVPS to grow by 6.2% to $45.92, mediocre growth rate.

Key Takeaways from Prosperity Bancshares’s Q3 Results

We struggled to find many positives in these results. Its net interest income slightly missed and its EPS was in line with Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 2% to $62.01 immediately following the results.

Prosperity Bancshares may have had a tough quarter, but does that actually create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.