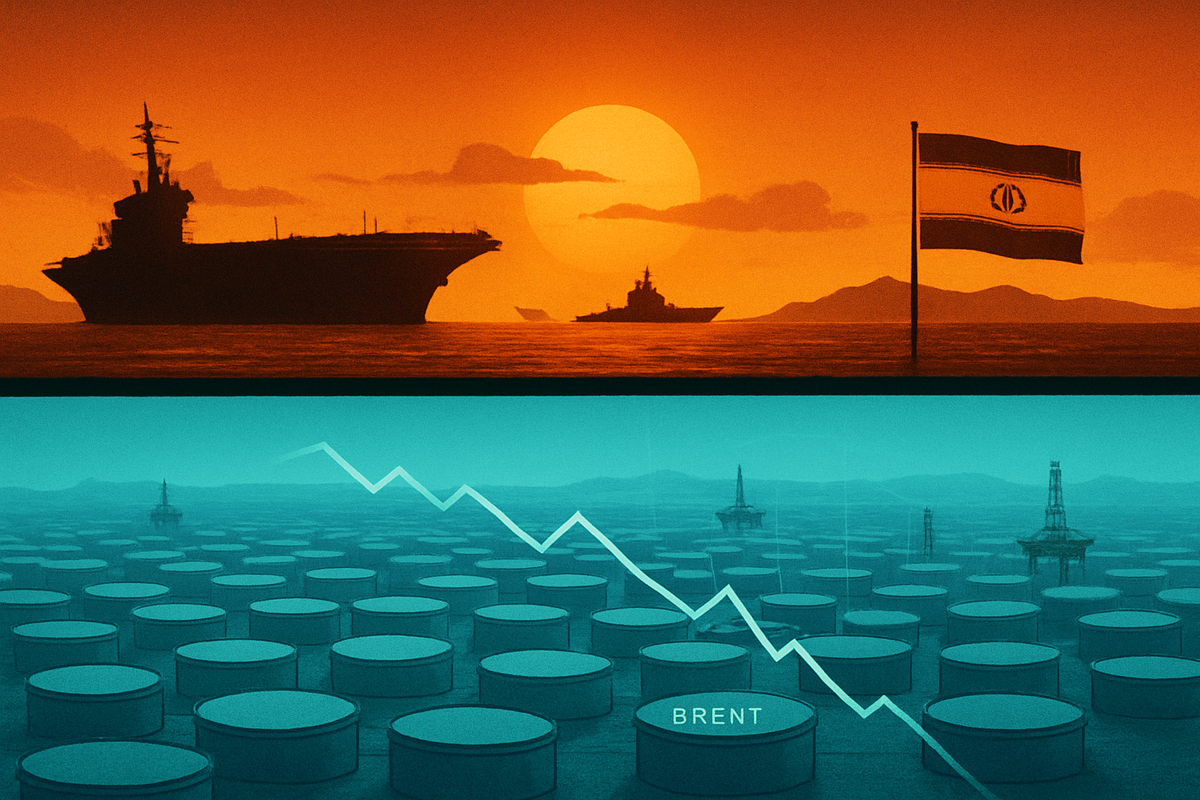

As of February 27, 2026, the global energy landscape is caught in a high-stakes tug-of-war between volatile Middle Eastern diplomacy and the cold reality of overproduction. Brent crude is currently averaging $63 per barrel for the first quarter of 2026, a price point buoyed significantly by a "risk premium" stemming from escalating tensions between the United States and Iran. While the specter of conflict has kept prices from collapsing, market analysts warn that a deepening fundamental surplus is waiting in the wings to pull the rug out from under energy bulls.

The current market equilibrium is fragile. While spot prices have seen intermittent spikes toward the $70 mark on news of military posturing, the underlying average remains tethered to the low 60s. Investors are increasingly looking toward the Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (NASDAQ: PDBC) as a barometer for how these conflicting forces—geopolitical fear versus physical oversupply—are being priced into the broader commodity complex.

The Geneva Standoff and the Strait of Hormuz Shadow

The primary driver of the current $63 average is the deteriorating state of indirect nuclear negotiations between Washington and Tehran in Geneva. Throughout January and February 2026, these talks have hit several "dead ends," leading to heightened military rhetoric. Analysts at major financial institutions estimate that a geopolitical risk premium of $4 to $10 per barrel is currently baked into the price of Brent crude. Without the fear of a potential U.S. strike on Iranian nuclear facilities or a retaliatory closure of the Strait of Hormuz—a transit point for 20% of the world's oil—prices would likely be trading in the mid-50s.

The timeline leading to this friction began in late 2025, when a series of maritime "shadow war" incidents in the Persian Gulf reignited fears of supply disruptions. By early 2026, Iran had ramped up its crude shipments to record levels, attempting to move as much inventory as possible into floating storage or to friendly buyers before any potential new round of secondary sanctions could take full effect. This surge in Iranian exports has paradoxically contributed to the very surplus that is now capping the upside of the geopolitical rally.

Energy Giants and ETFs Navigating the Volatility

The current environment presents a mixed bag for major oil producers and investment vehicles. Integrated energy giants like Exxon Mobil Corporation (NYSE: XOM) and Chevron Corporation (NYSE: CVX) are benefiting from the short-term price support provided by the risk premium, which helps sustain their aggressive dividend and buyback programs. However, these companies are also facing the reality of a 1 million barrel per day (bpd) global surplus expected for the remainder of 2026. For companies with significant North American shale exposure, such as Occidental Petroleum Corporation (NYSE: OXY), the $63 Brent price is comfortably above the break-even point but leaves little room for error if the geopolitical premium evaporates.

For diversified investors, the Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (NASDAQ: PDBC) has become a focal point. As of late February 2026, the fund has seen a year-to-date gain of roughly 9%, largely driven by its heavy weighting in energy and industrial metals. Following a January rebalance, the fund increased its Brent crude exposure to a record 8.36% of its commodity basket. While the ETF’s "optimum yield" strategy helps mitigate the costs of rolling futures contracts, the fund remains vulnerable to a sharp correction if the predicted 2026 supply glut overwhelms the current geopolitical narrative.

The Looming Glut: Supply vs. Strategy

Beyond the headlines of the Geneva talks, a more persistent threat to oil prices is emerging: a massive global supply surplus. The International Energy Agency (IEA) has consistently forecast an average surplus of just under 1 million bpd for 2026. This oversupply is being driven by robust production growth in non-OPEC+ nations, specifically the United States, Brazil, and Guyana. This surge in production is colliding with a slowing growth rate in global oil demand as the "energy transition" begins to bite into traditional fuel consumption patterns.

Historically, such a surplus would lead to a rapid price collapse, but two factors are currently acting as a safety net. First, OPEC+, led by Saudi Arabia and Russia, has opted to hold production steady through the first quarter of 2026, deferring planned increases to monitor the U.S.-Iran situation. Second, China has been aggressively utilizing low-60s prices to bolster its strategic reserves, effectively soaking up nearly 1 million bpd of excess supply. Should China reach its storage capacity or OPEC+ lose its discipline, the 1 million bpd surplus will hit the market with full force, likely driving Brent toward the $50 mark.

Strategic Pivots in a "Higher for Not-Much-Longer" Market

Looking ahead to the second half of 2026, the market faces two distinct scenarios. In the first, a diplomatic breakthrough in Geneva could remove the risk premium overnight, causing a sharp "flush out" of long positions and a rapid descent in prices. In the second, a military escalation could see prices briefly spike toward $100 before the sheer weight of the global surplus and the potential for a global economic slowdown bring prices back down to earth.

Strategic players are already positioning for these outcomes. European majors like Shell PLC (NYSE: SHEL) and BP PLC (NYSE: BP) are continuing to pivot their capital expenditures toward low-carbon energy and natural gas, hedging against a long-term decline in crude profitability. Meanwhile, U.S. independent producers are focusing on capital discipline, prioritizing "value over volume" to ensure they can remain profitable even if the $63 average proves to be the high-water mark for the year.

Summary and Investor Outlook

The first quarter of 2026 has defined a new "normal" for the oil market: a state of permanent tension where geopolitical fear is the only thing standing between the current price and a fundamental bear market. The $63 Brent average is a compromise price—high enough to keep producers profitable, but low enough to reflect the looming 1 million bpd surplus.

For investors, the coming months require a focus on "tail risks." While the PDBC ETF offers a way to play the current commodity strength, the risk of a "peace dividend" or a "surplus shock" is high. Watch for the next round of OPEC+ meetings in June and any signs that China is slowing its strategic stockpiling. In a market where 1 million barrels can make or break a price floor, the transition from Q1's geopolitical anxiety to Q3's fundamental reality will be the defining story of the year.

This content is intended for informational purposes only and is not financial advice.