Bolingbrook, Illinois-based Ulta Beauty, Inc. (ULTA) is a beauty retailer that offers branded and private label beauty products, including prestige and mass-market cosmetics, fragrances, skincare, and haircare products. Valued at a market cap of $22.9 billion, the company also provides beauty services, including hair, makeup, brow, and skin services at its stores.

Companies worth $10 billion or more are typically classified as “large-cap stocks,” and ULTA fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the specialty retail industry. For fiscal 2026, the firm is prioritizing international growth in Mexico and the Middle East, a high-profile integration with TikTok Shop, and the rollout of its curated online Marketplace.

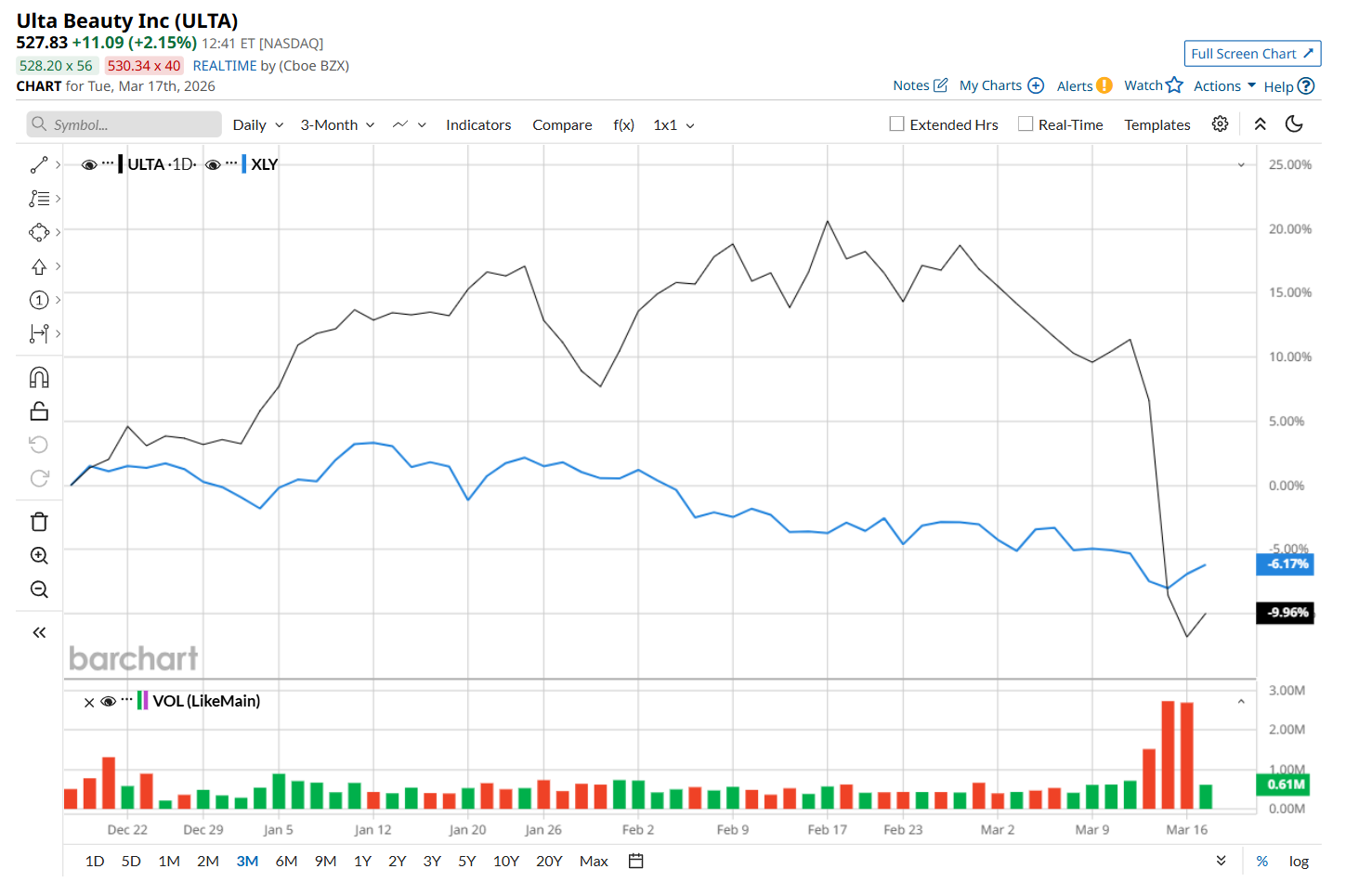

This beauty retailer has dipped 25.8% from its 52-week high of $714.97, reached on Feb. 18. Shares of ULTA have declined 9.4% over the past three months, underperforming the State Street Consumer Discretionary Select Sector SPDR ETF’s (XLY) 6.1% drop during the same time frame.

Moreover, on a YTD basis, shares of ULTA are down 12.5%, compared to XLY’s 5.4% fall. Nonetheless, in the longer term, ULTA has soared 48.3% over the past 52 weeks, considerably outpacing XLY’s 14.7% uptick over the same time frame.

To confirm its recent bearish trend, ULTA has started trading below its 200-day moving average since mid-March, and has remained below its 50-day moving average since early March.

On Mar. 12, ULTA delivered its Q4 earnings results, and its shares crashed 14.2% in the following trading session. The company’s net sales increased 11.8% year-over-year to $3.9 billion, topping consensus estimates by 2.4%. However, its operating income margin contracted by 260 basis points from the year-ago quarter to 12.2%, which might have raised investor concerns over profitability. Meanwhile, despite an increase in revenue, its EPS fell 5.3% from the same period last year to $8.01, meeting analyst expectations.

ULTA has notably outperformed its rival, Bath & Body Works, Inc. (BBWI), which declined 33.1% over the past 52 weeks. However, it has lagged BBWI’s slight YTD rise.

Despite ULTA’s recent underperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 25 analysts covering it, and the mean price target of $691.04 suggests a 30.9% premium to its current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart