The debut of PayPay Corporation (PAYP) has quickly become one of the most closely watched fintech stories of 2026, and not just because of its strong IPO pop. Backed by SoftBank Group (SFTBY), the digital payments giant went public on March 12 and surged after pricing its Nasdaq listing at $16 and opening around $19, signaling robust investor appetite despite a volatile macro backdrop.

Now, the narrative has taken another bullish turn as star investor Cathie Wood has stepped in. Through ARK’s fintech-focused ETF, ARK Blockchain & Fintech Innovation ETF (ARKF), Wood snapped up 275,000 shares, worth roughly $5 million on day one, reflecting an early vote of confidence in PayPay’s long-term disruption potential in global digital payments.

With PayPay boasting over 70 million users and $100 billion in gross merchandise volume and positioning itself as a “super app” spanning payments, banking, and lending, its public debut arrives at a time when investors are once again hunting for the next big fintech winner.

So, if Cathie Wood is buying into this newly public fintech, should you follow suit?

About PayPay Stock

PayPay Corporation is a Japan-based digital payments and fintech company headquartered in Chiyoda, Tokyo, and is majority-owned by SoftBank Group. Founded in 2018, the company operates one of Japan’s largest mobile payment platforms, offering QR code–based payments alongside expanding financial services such as lending and banking. Following its U.S. listing, PayPay commands a market cap of roughly $12.9 billion.

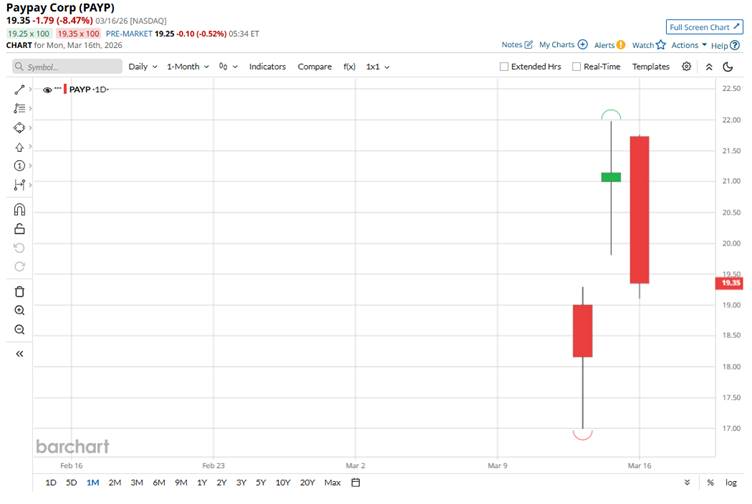

PayPay Corporation’s stock price performance since its Nasdaq debut has reflected a strong initial reception. The company priced its IPO at $16 per share on March 12, a level set below its marketed range due to broader market volatility and geopolitical uncertainty. Despite the conservative pricing, investor demand proved robust, with the stock opening around $19, representing a nearly 19% immediate gain and signaling solid institutional appetite for the offering.

In the days following its debut, PayPay shares are largely held above the IPO price. The last closing was at $19.77, after a 8.5% intraday slump, while overall gains since the debut stand at 6.6%.

The stock is currently trading at 5.23 times sales, which is higher than the sector median of 2.97 times.

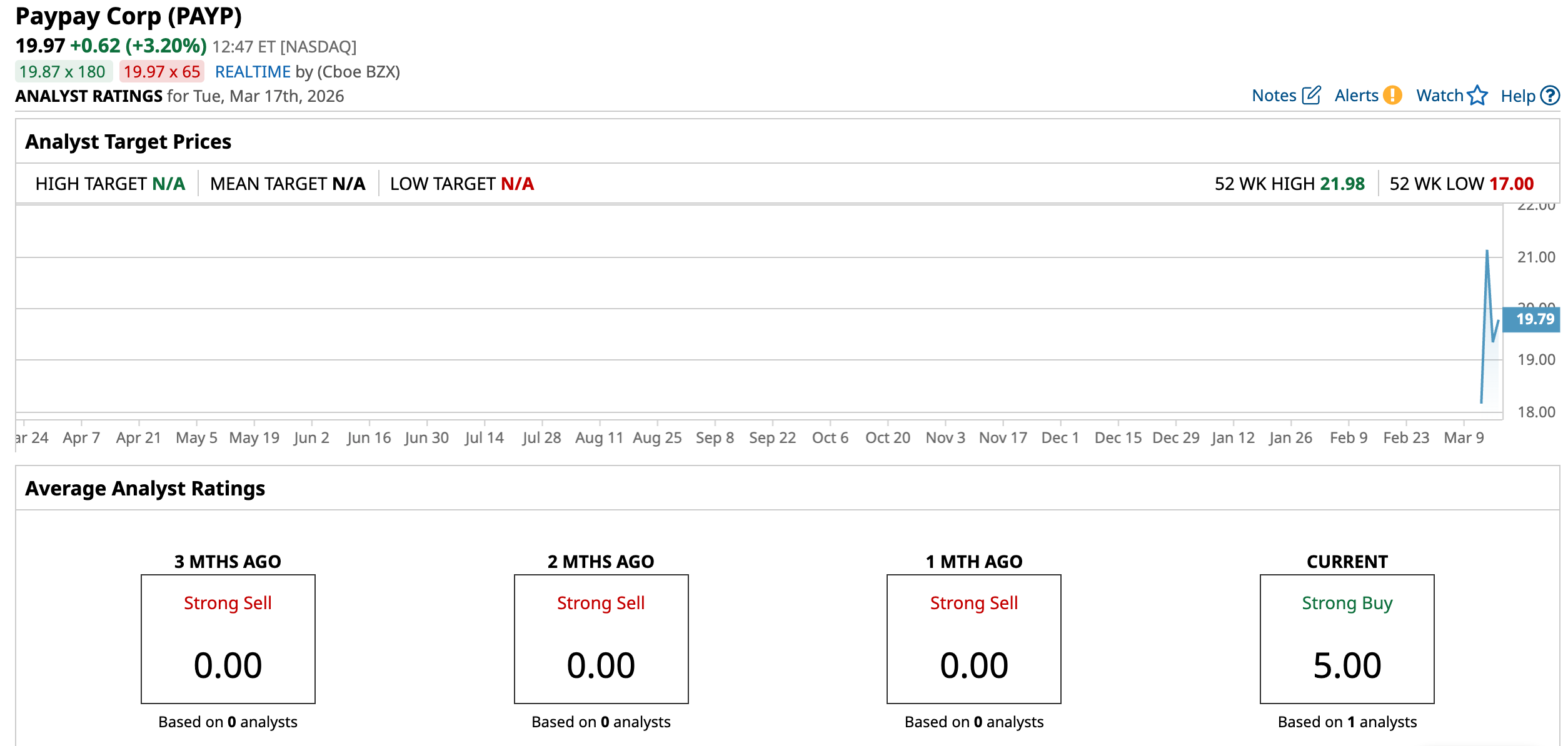

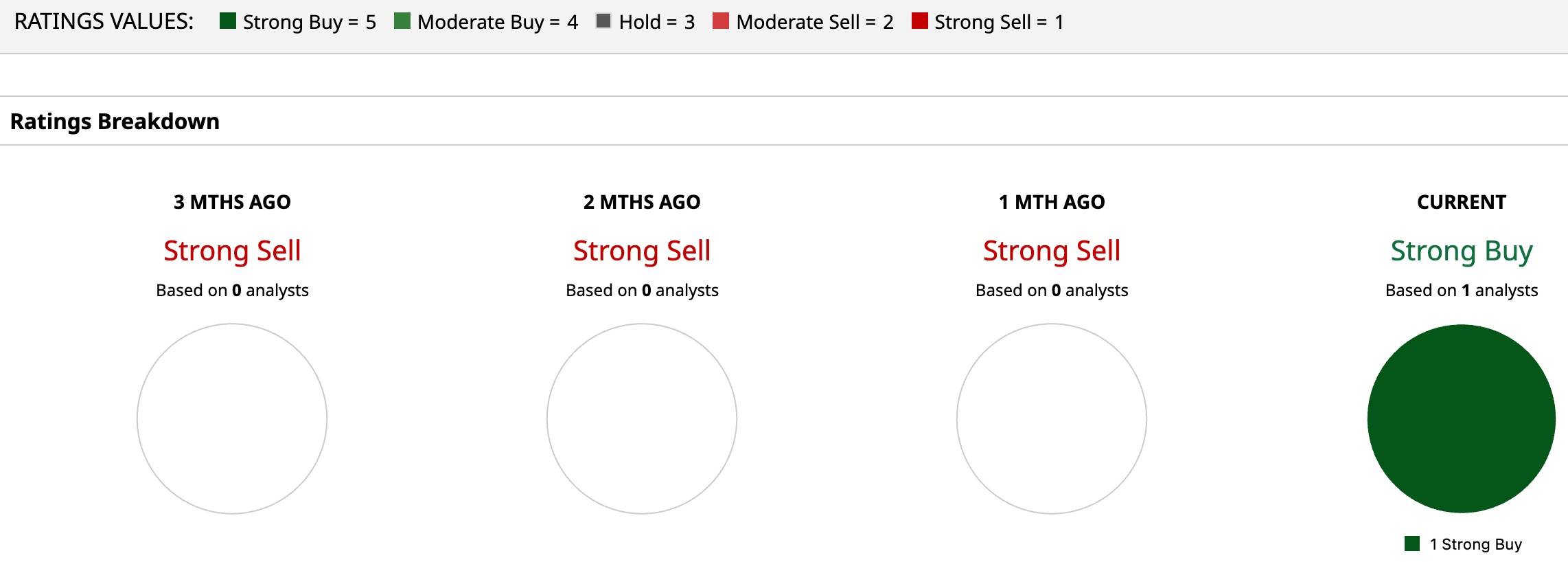

Analysts are Turning Optimistic While Cathie Wood Makes a Bold Early Bet

Analyst expectations for PayPay Corporation are beginning to skew positively as formal coverage emerges following its IPO, with early indications pointing to meaningful upside potential driven by its scale and positioning in Japan’s digital payments ecosystem.

The most prominent initiation has come from Macquarie, which launched coverage with an “Outperform” rating and a $22.90 price target. This target implies solid upside, reflecting confidence in PayPay’s ability to leverage its massive user base and transition into a higher-margin fintech platform. The bullish thesis is underpinned by structural growth in cashless adoption across Japan, as well as PayPay’s evolution into a broader “super app” integrating payments, lending, and financial services.

Meanwhile, Cathie Wood has taken a clear bullish stance. Her investment reflects a thematic bet on the continued rise of mobile wallets, embedded finance, and platform-driven ecosystems, reinforcing the broader bullish narrative around the company.

With a leading position in Japan’s fintech landscape, strong early trading momentum, and backing from both institutional analysts like Macquarie and high-profile investors like Cathie Wood, PayPay can be viewed as a high-growth fintech platform with meaningful upside potential as it scales its strategy.

Overall, CRM boasts a consensus “Strong Buy” rating currently.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart