I know, I know. Short-term bonds? As great investments? Blasphemy, right? But hear me out. I think there’s more than a puncher’s chance that among all of those fancy covered call option ETFs, closed-end funds with double-digit yields, and dividend stocks “due” for a rebound in 2026, the year might belong to some of the most boring ETFs on planet earth.

I’ll name names below. First, allow me to make the case for why ETFs owning U.S. Treasury securities with maturities between 1-7 years might just surprise some folks in 2026.

The economy heading into the new year is a tossup. At least if you listen to all of the financial chatter I do on a daily basis. One thing that concerns me is that the same people bragging about how great the economy is also want a stimulative rate cut? What are we even doing here?

I’m a technician, and don’t buy into political or even broad economic approaches to assessing the markets. I look at pictures all day. Pictures of price trends, in stocks and ETFs, as well as the market “headline” indexes. And what I see is high risk for the stock market. And a push from enough big-money sources to guide short-term interest rates down.

So to summarize, there are two different reasons short-term U.S. rates can decline in 2026, perhaps significantly.

- The “we need lower rates” crowd wants it, and has the potential to get it. That’s a mix of government officials who have a boatload of T-bills maturing in the next 12 months that need refinancing, and investors who want QE infinity (cheap money forever, the better to speculate with). And with a new Fed chair coming soon, there’s the will to do it.

- If the economy slips into recession (a word not uttered enough these days in my view, given the K-shaped economy in progress), that alone will be an easy path to lower rates. To stimulate the economy because it really needs it, not because Wall Street folks need to borrow more to leverage more.

So, that’s my case in brief. And while stocks and longer-term bonds are potentially winners in that scenario, they both come with more risk than ETFs like this pair, and others like them.

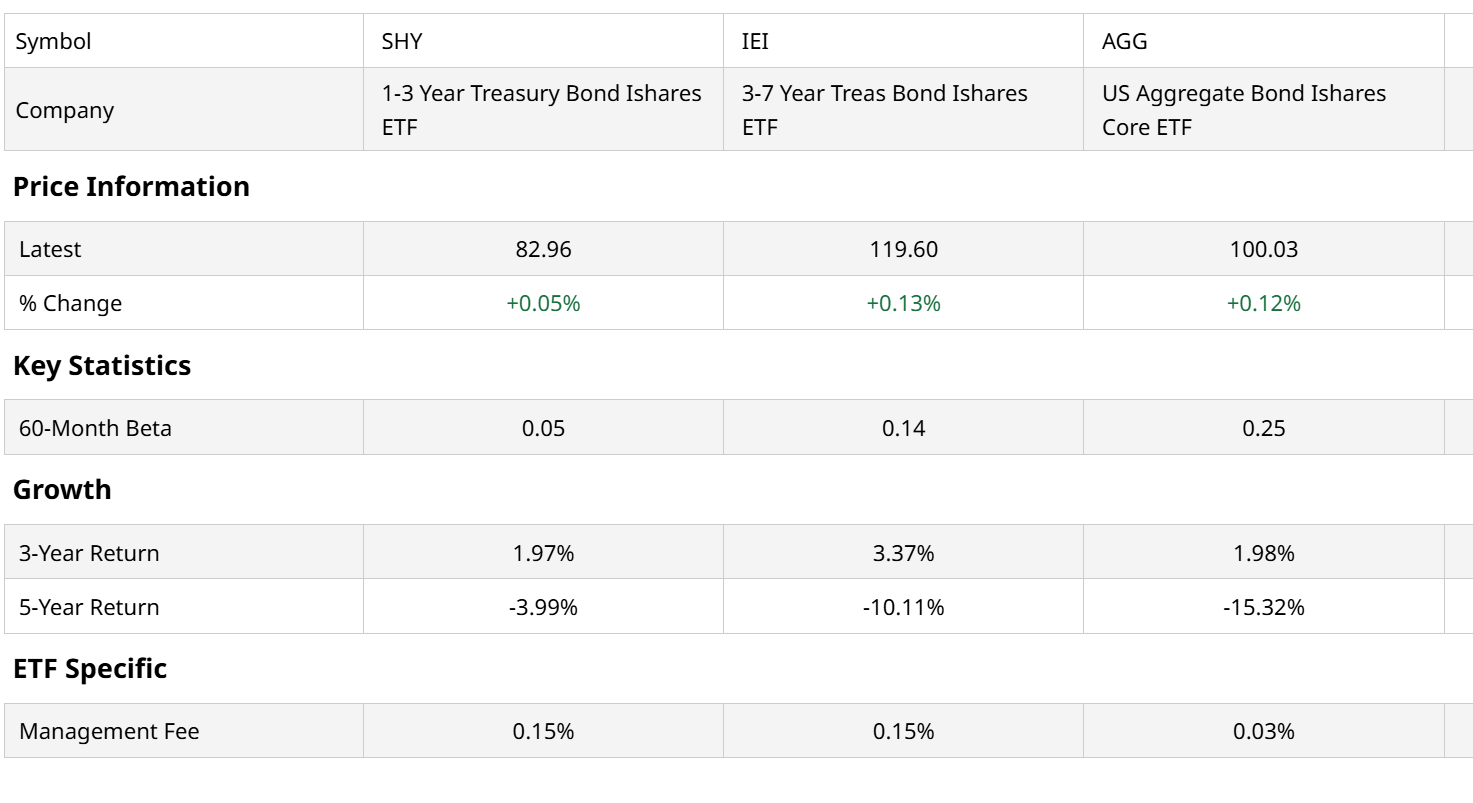

The two I’m focusing on are 1-3 Year Treasury Bond iShares (SHY) and 3-7 Year Treasury Bond iShares (IEI). They are both in my unofficial “ETF hall of fame” for how they bailed me out in past market cycles.

I am a big fan of inverse ETFs, which help us to profit directly from falling stock prices. But this pair, when conditions are right, as they might be in 2026, have all of this going for them:

- Long-tenured (SHY debuted in 2002, IEI in 2007). They have stood up through some rough stock and bond markets.

- Low cost (puny expense ratios, so that doesn’t get in the way)

- Less volatile by nature, given the shorter maturities. I compared them both in the table above to a standard bond benchmark.

- High quality. The U.S. government’s bond rating may no longer be AAA, but if it can’t pay us back on debt like this, I think we have bigger, more widespread issues as investors.

- Total return potential from lower rates

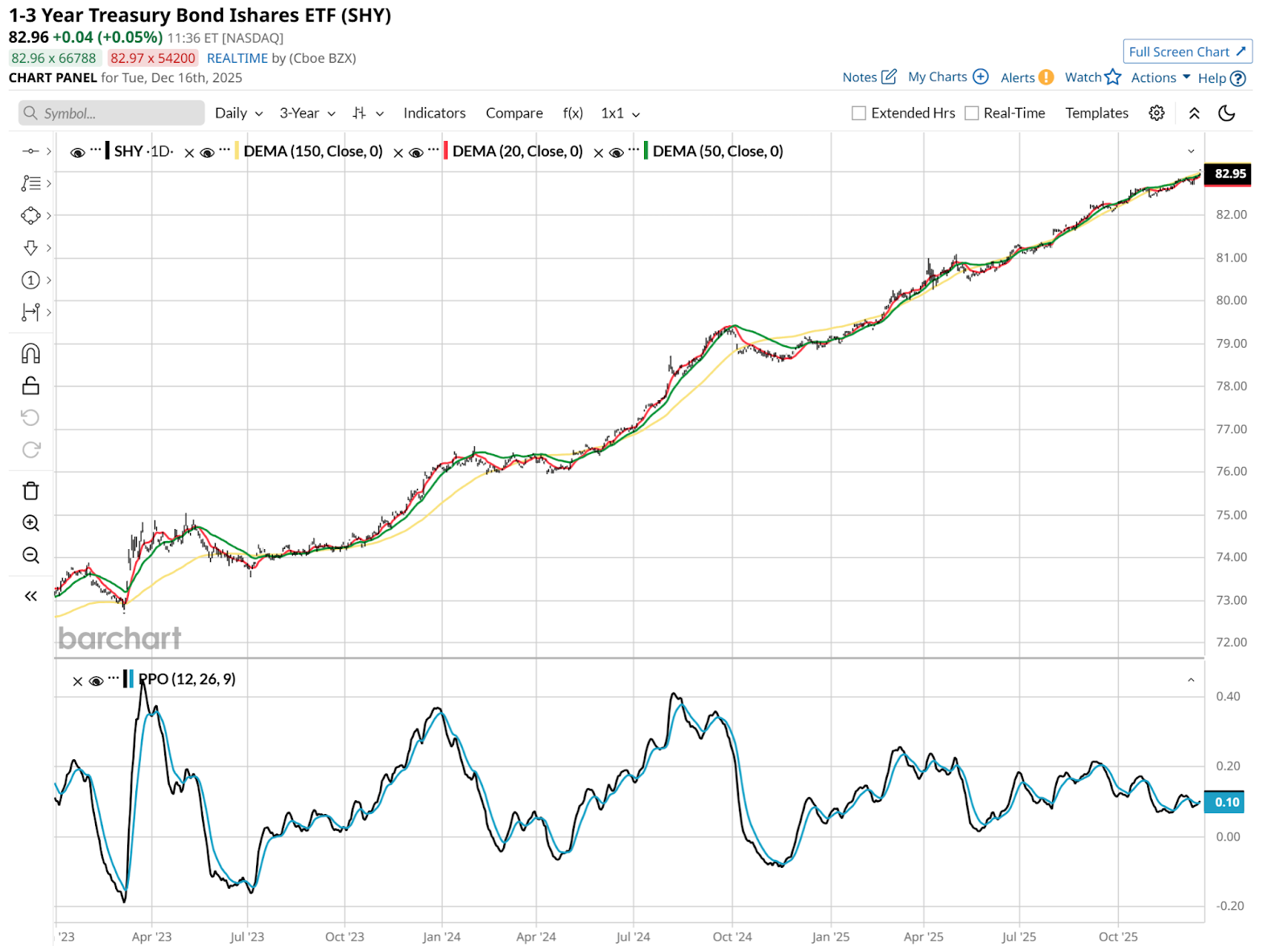

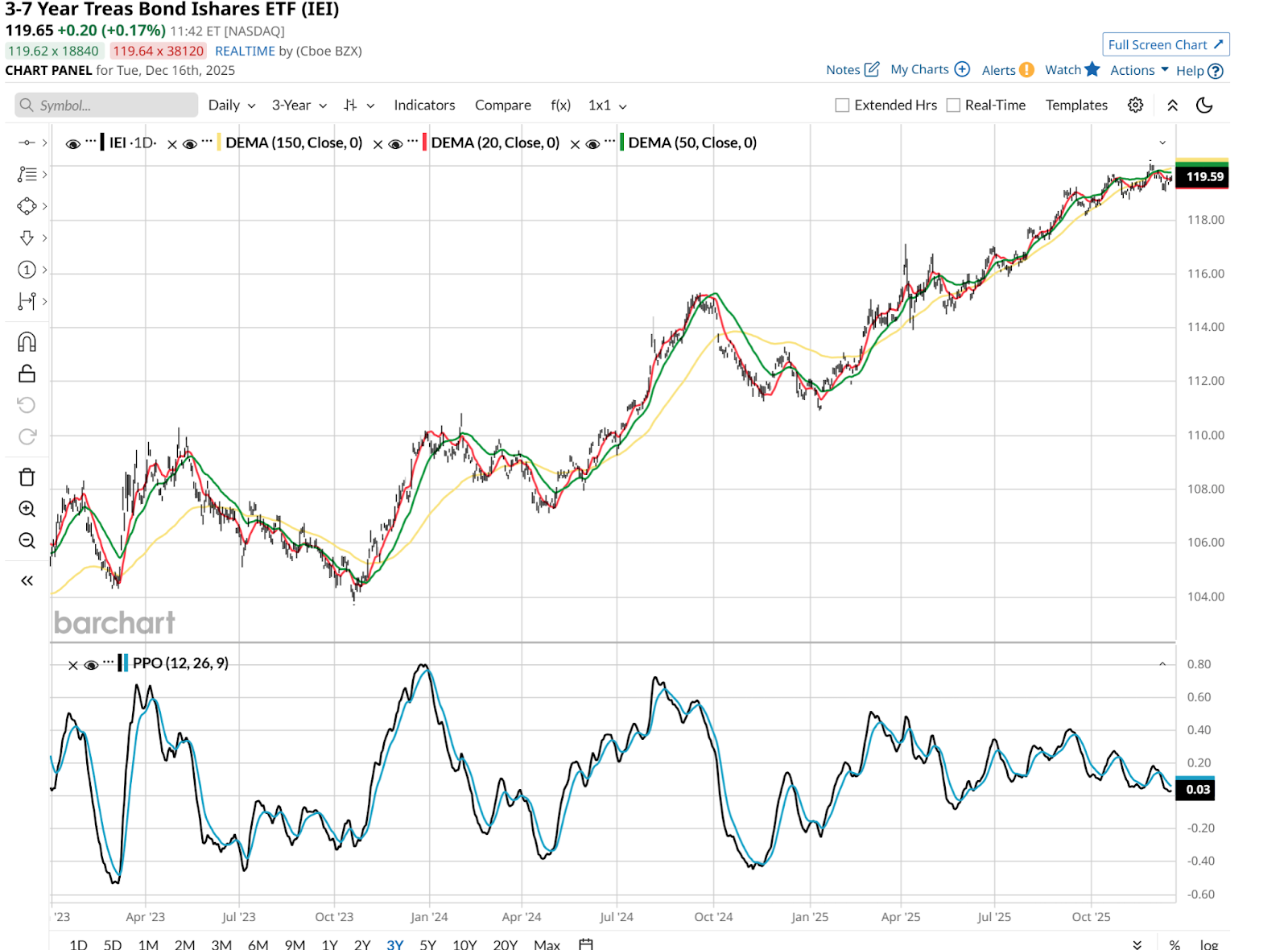

Let’s explore that last one. These two ETFs don’t move around in price much. Check out their betas in that table above. But they will appreciate in price if rates fall.

That, plus their present yields of around 3.2%-3.4%, looks uninspiring after a year like we’ve had for stocks. But put the price gains and that starting yield together, an in a down slide for stocks and perhaps an increase in the long end of the yield curve, SHY and IEI could fill a gap. The gap between the ultra-safety but no price appreciation of T-bills, and the wild west of everything else in a market disruption.

In other words, a chart like this will suddenly look very desirable. IEI has a bit more price action, which also means that if rates decline out to its 3-7 year maturity range, it can add a few percentage points to that 3%-4% yield over a year’s time

Looking at ETFs like this is something akin to a combination of risk management and cash management. It is not likely the moment in the market cycle where “everyone” will be clamoring for ideas like this.

But if history rhymes, there will come a time when you’ll be glad you bookmarked this article.

Rob Isbitts, founder of Sungarden Investment Publishing, is a semi-retired chief investment officer, whose current research is found here at Barchart, and at his ETF Yourself subscription service on Substack. To copy-trade Rob’s portfolios, check out the new Pi Trade app.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart