Over the past six months, Royal Caribbean’s shares (currently trading at $309.20) have posted a disappointing 6.1% loss, well below the S&P 500’s 7.6% gain. This may have investors wondering how to approach the situation.

Is now the time to buy Royal Caribbean, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Royal Caribbean Will Underperform?

Even with the cheaper entry price, we're sitting this one out for now. Here are three reasons why RCL doesn't excite us and a stock we'd rather own.

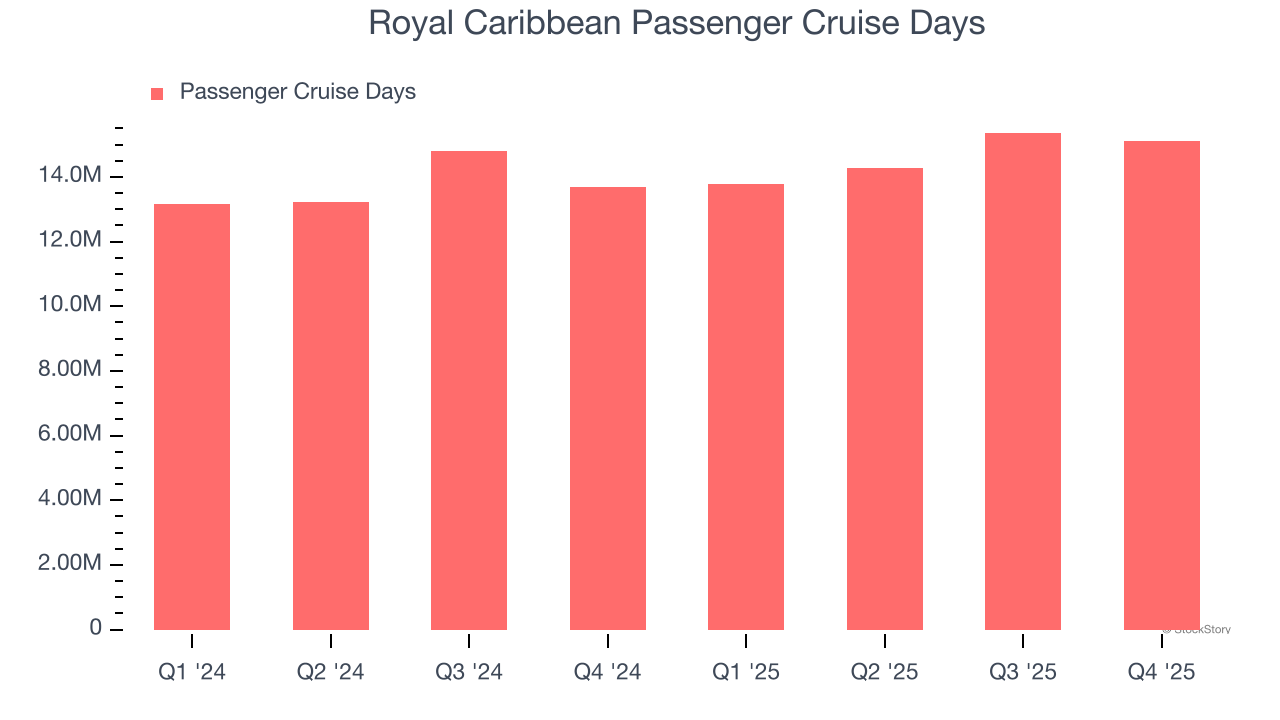

1. Weak Growth in Passenger Cruise Days Points to Soft Demand

Revenue growth can be broken down into changes in price and volume (for companies like Royal Caribbean, our preferred volume metric is passenger cruise days). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Royal Caribbean’s passenger cruise days came in at 15.12 million in the latest quarter, and over the last two years, averaged 6.7% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

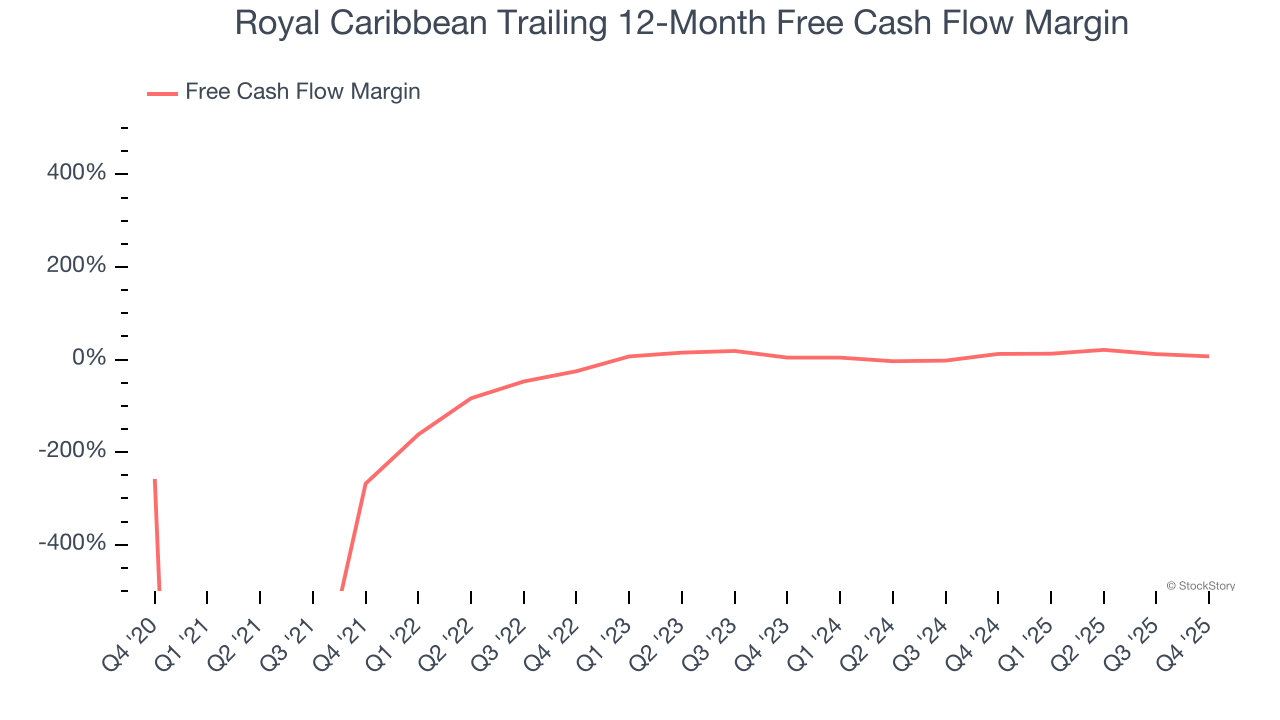

2. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Royal Caribbean has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 9.4%, lousy for a consumer discretionary business.

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Royal Caribbean historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 4.7%, lower than the typical cost of capital (how much it costs to raise money) for consumer discretionary companies.

Final Judgment

Royal Caribbean falls short of our quality standards. After the recent drawdown, the stock trades at 17.6× forward P/E (or $309.20 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are more exciting stocks to buy at the moment. We’d suggest looking at one of our all-time favorite software stocks.

High-Quality Stocks for All Market Conditions

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.