As the craze of earnings season draws to a close, here’s a look back at some of the most exciting (and some less so) results from Q2. Today, we are looking at sit-down dining stocks, starting with Darden (NYSE: DRI).

Sit-down restaurants offer a complete dining experience with table service. These establishments span various cuisines and are renowned for their warm hospitality and welcoming ambiance, making them perfect for family gatherings, special occasions, or simply unwinding. Their extensive menus range from appetizers to indulgent desserts and wines and cocktails. This space is extremely fragmented and competition includes everything from publicly-traded companies owning multiple chains to single-location mom-and-pop restaurants.

The 12 sit-down dining stocks we track reported a mixed Q2. As a group, revenues beat analysts’ consensus estimates by 1% while next quarter’s revenue guidance was 5.4% below.

While some sit-down dining stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 2.8% since the latest earnings results.

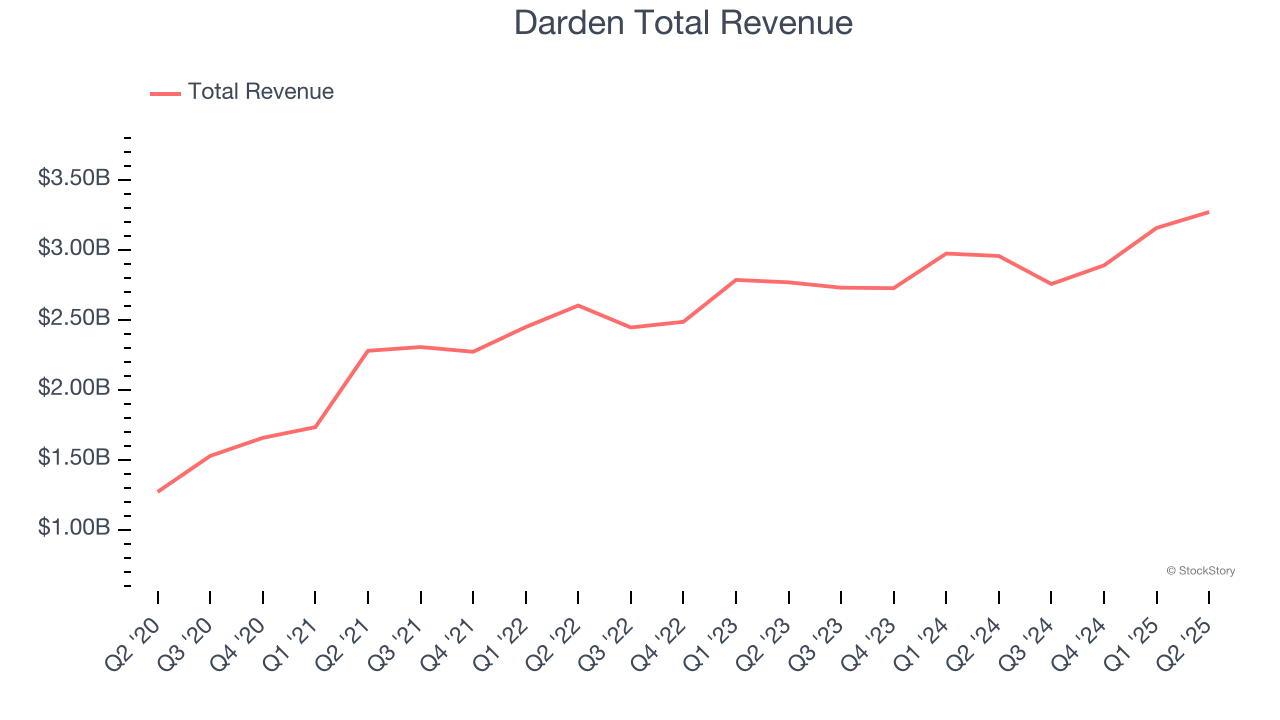

Darden (NYSE: DRI)

Founded in 1968 as Red Lobster, Darden (NYSE: DRI) is a leading American restaurant company that owns and operates a portfolio of popular restaurant brands.

Darden reported revenues of $3.27 billion, up 10.6% year on year. This print was in line with analysts’ expectations, but overall, it was a mixed quarter for the company with an impressive beat of analysts’ same-store sales estimates but a significant miss of analysts’ EPS estimates.

"We had a strong quarter with same-restaurant sales and earnings growth that exceeded our expectations," said Darden President & CEO Rick Cardenas.

Unsurprisingly, the stock is down 5.5% since reporting and currently trades at $210.48.

Is now the time to buy Darden? Access our full analysis of the earnings results here, it’s free.

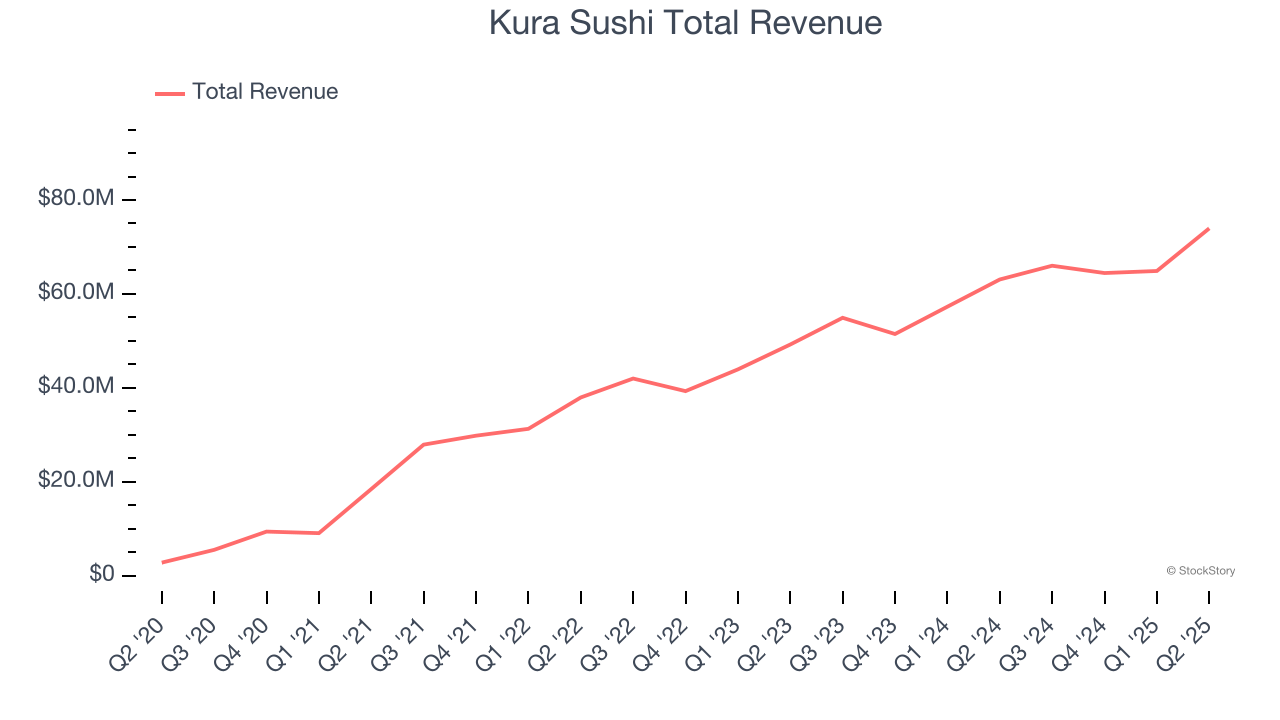

Best Q2: Kura Sushi (NASDAQ: KRUS)

Known for its conveyor belt that transports dishes to diners, Kura Sushi (NASDAQ: KRUS) is a chain of sushi restaurants serving traditional Japanese fare with a touch of modernity and technology.

Kura Sushi reported revenues of $73.97 million, up 17.3% year on year, outperforming analysts’ expectations by 2.5%. The business had a very strong quarter with a beat of analysts’ EPS and EBITDA estimates.

Kura Sushi delivered the highest full-year guidance raise among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 10.3% since reporting. It currently trades at $77.80.

Is now the time to buy Kura Sushi? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Bloomin' Brands (NASDAQ: BLMN)

Owner of the iconic Australian-themed Outback Steakhouse, Bloomin’ Brands (NASDAQ: BLMN) is a leading American restaurant company that owns and operates a portfolio of popular restaurant brands.

Bloomin' Brands reported revenues of $1.00 billion, down 10.4% year on year, exceeding analysts’ expectations by 1.4%. Still, it was a softer quarter as it posted full-year EPS guidance missing analysts’ expectations.

Bloomin' Brands delivered the slowest revenue growth in the group. As expected, the stock is down 23.2% since the results and currently trades at $6.90.

Read our full analysis of Bloomin' Brands’s results here.

Texas Roadhouse (NASDAQ: TXRH)

With locations often featuring Western-inspired decor, Texas Roadhouse (NASDAQ: TXRH) is an American restaurant chain specializing in Southern-style cuisine and steaks.

Texas Roadhouse reported revenues of $1.51 billion, up 12.7% year on year. This result beat analysts’ expectations by 0.6%. More broadly, it was a mixed quarter as it also produced an impressive beat of analysts’ same-store sales estimates but a miss of analysts’ EBITDA estimates.

The stock is down 10.8% since reporting and currently trades at $165.05.

Read our full, actionable report on Texas Roadhouse here, it’s free.

The Cheesecake Factory (NASDAQ: CAKE)

Celebrated for its delicious (and free) brown bread, gigantic portions, and delectable desserts, Cheesecake Factory (NASDAQ: CAKE) is an iconic American restaurant chain that also owns and operates a portfolio of separate restaurant brands.

The Cheesecake Factory reported revenues of $955.8 million, up 5.7% year on year. This print surpassed analysts’ expectations by 0.8%. Overall, it was a strong quarter as it also recorded a solid beat of analysts’ EBITDA and EPS estimates.

The stock is down 12.8% since reporting and currently trades at $55.06.

Read our full, actionable report on The Cheesecake Factory here, it’s free.

Market Update

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty for 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.